Managing a middle-class family budget in India is getting harder every year.

Rent is rising. Grocery bills keep increasing. School fees never stop. One medical emergency can destroy monthly savings.

Most families are not overspending on luxury. They are leaking money through small daily expenses.

This guide breaks down a realistic monthly expense structure for Indian middle-class families. You’ll learn how much families usually spend, where money gets wasted, and how to build a practical budget without living miserably.

Quick Answer: Monthly Expense Breakdown for Middle-Class Families in India

A typical middle-class Indian family spends money like this:

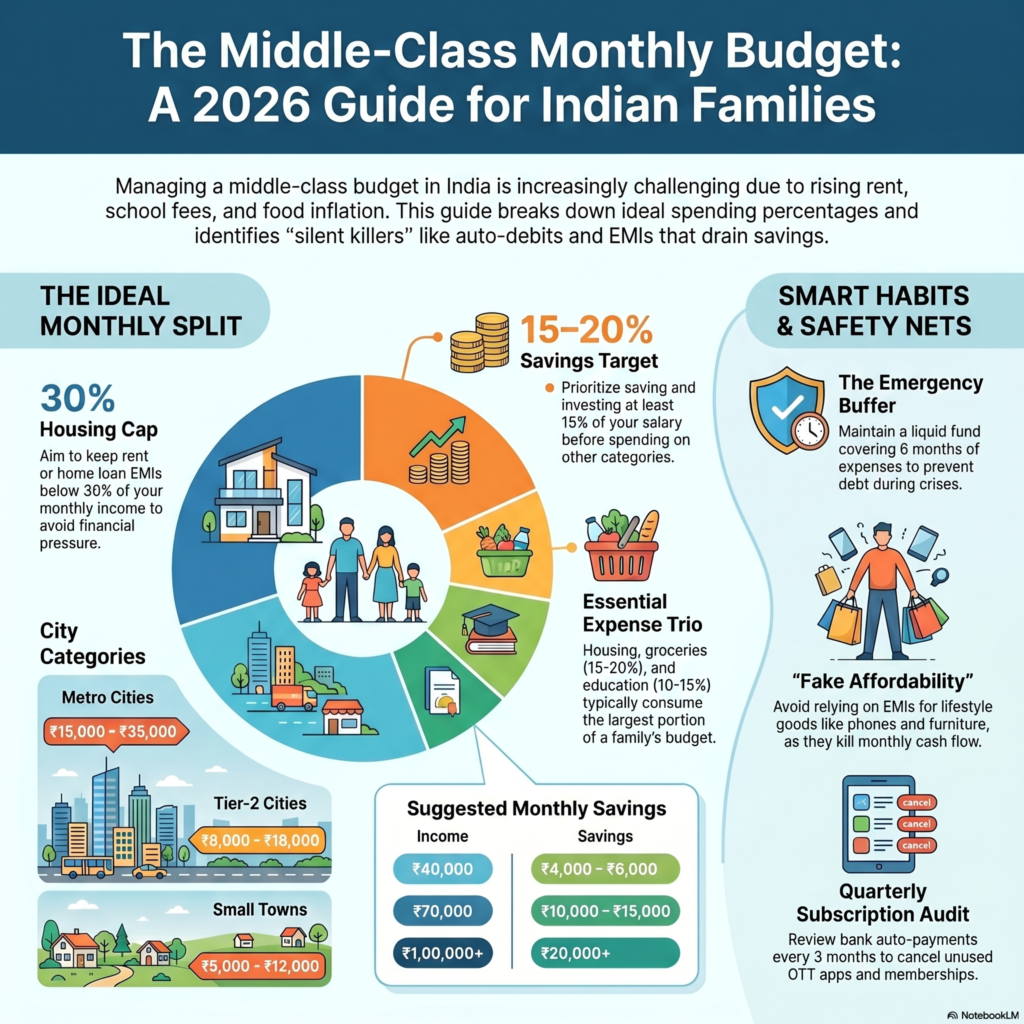

- 25–35% on rent or home loan

- 15–20% on groceries and food

- 10–15% on education and children

- 8–12% on transport and fuel

- 5–10% on medical and insurance

- 10–20% on savings and investments

- Remaining on utilities, EMIs, entertainment, and emergencies

For a family earning ₹80,000 monthly, expenses usually range between ₹60,000–₹70,000.

What Is a Healthy Monthly Expense Breakdown?

A monthly expense breakdown simply means dividing income into categories.

Most Indian families don’t track spending properly. They only check bank balance.

That’s the problem.

If you don’t know where money goes, salary disappears automatically.

A proper budget helps you:

- Avoid unnecessary debt

- Build emergency savings

- Reduce stress

- Plan long-term goals

- Invest consistently

You do not need complicated spreadsheets.

You need awareness and discipline.

Monthly Expense Breakdown for Middle-Class Families in India

1. House Rent or Home Loan EMI

This is usually the biggest expense.

For most families, housing takes 25–35% of income.

Typical Monthly Cost

| City Type | Average Rent |

| Metro cities | ₹15,000–₹35,000 |

| Tier-2 cities | ₹8,000–₹18,000 |

| Small towns | ₹5,000–₹12,000 |

Why It Matters

Many families make one mistake.

They choose status over affordability.

A bigger apartment often means:

- Less savings

- More debt

- Higher maintenance costs

Best Rule

Keep rent below 30% of monthly income.

Example

If family income is ₹70,000:

- Ideal rent = ₹18,000–₹21,000

Not ₹35,000.

2. Grocery and Food Expenses

Food costs have increased sharply in India.

Especially after inflation in cooking oil, vegetables, milk, and packaged foods.

Average Monthly Grocery Cost

| Family Size | Monthly Grocery Budget |

| Couple | ₹6,000–₹10,000 |

| Family with 1 child | ₹10,000–₹18,000 |

| Larger family | ₹18,000+ |

What Increases Food Spending?

- Swiggy and Zomato orders

- Daily snacks

- Buying branded products unnecessarily

- Wasting groceries

Smart Action

Use UPI cashback apps and supermarket offers carefully.

But don’t fall for fake “discount savings” by buying things you never needed.

3. Utilities and Bills

These are silent budget killers.

Small recurring bills become huge yearly expenses.

Common Monthly Bills

- Electricity

- Internet

- Mobile recharge

- Gas cylinder

- Water charges

- OTT subscriptions

Typical Monthly Cost

₹3,000–₹8,000 depending on lifestyle.

Common Problem

People ignore auto-debits.

Then suddenly:

- 5 OTT subscriptions

- Premium apps

- Unused memberships

All draining money monthly.

Action Step

Review bank auto-payments every 3 months.

Cancel useless subscriptions immediately.

4. Education Expenses

School fees are crushing middle-class families now.

Especially in private schools.

Typical Education Costs

| Expense | Monthly Estimate |

| School fees | ₹3,000–₹15,000 |

| Tuition | ₹2,000–₹8,000 |

| Books & supplies | ₹1,000–₹3,000 |

Reality Check

Many parents overspend for “premium” schools while ignoring financial stability.

Expensive school does not guarantee success.

Financial stress at home affects children more.

Better Approach

Focus on:

- Good teaching

- Child’s environment

- Skill development

- Savings for higher education

Not brand-name schools alone.

Monthly Expense Breakdown for Middle-Class Families in India: Transport Costs

Transport expenses vary heavily by city.

Common Costs

- Petrol

- Bike EMI

- Car EMI

- Maintenance

- Metro or bus pass

- Ola/Uber rides

Average Spending

₹4,000–₹12,000 monthly.

Biggest Mistake

Buying cars too early.

A car is not an investment.

For many middle-class families, it becomes a long-term cash drain.

Better Strategy

Buy a car only if:

- Emergency fund exists

- Insurance is covered

- EMI stays manageable

Otherwise, public transport and two-wheelers make more financial sense.

Insurance and Medical Expenses

This category becomes important only after disaster.

That’s why most people ignore it.

Then one hospital bill destroys years of savings.

Minimum Protection Every Family Needs

Health Insurance

Family floater plans are important.

Especially after age 30.

Popular options include:

Term Insurance

If one person depends on your income, term insurance is necessary.

Not investment-linked insurance plans.

Pure term plans.

Typical Monthly Budget

₹3,000–₹8,000 depending on age and coverage.

Savings and Investments

Most families save whatever remains.

That approach fails.

Savings should happen first.

Not last.

Good Monthly Savings Targets

| Income | Suggested Savings |

| ₹40,000 | ₹4,000–₹6,000 |

| ₹70,000 | ₹10,000–₹15,000 |

| ₹1 lakh | ₹20,000+ |

Simple Investment Options

SIP Mutual Funds

Easy for beginners.

Useful platforms:

Emergency Fund

Keep at least:

- 6 months of expenses

- In liquid savings or FD

Without emergency savings, every crisis becomes debt.

Real-Life Monthly Expense Breakdown for a Middle-Class Family in India

Example Scenario

Family:

- Husband

- Wife

- One child

City:

Chennai

Monthly family income:

₹85,000

Realistic Monthly Budget

| Expense Category | Monthly Amount |

| Rent | ₹20,000 |

| Groceries | ₹14,000 |

| School fees | ₹7,000 |

| Utilities | ₹4,500 |

| Petrol & transport | ₹6,000 |

| Insurance | ₹5,000 |

| SIP investments | ₹10,000 |

| Entertainment | ₹3,500 |

| Medical | ₹2,500 |

| Miscellaneous | ₹5,000 |

Total Expenses:

₹77,500

Remaining:

₹7,500

This is how most middle-class families actually live.

Not luxury.

Just survival with some savings.

Common Mistakes Middle-Class Families Make

1. Buying Things on EMI

EMIs create fake affordability.

Especially for:

- Phones

- Furniture

- Electronics

Too many EMIs kill cash flow.

2. Ignoring Insurance

People spend on gadgets first.

Insurance later.

That logic is financially dangerous.

3. No Expense Tracking

Without tracking:

- Spending increases silently

- Savings disappear

- Debt grows slowly

4. Depending Only on One Income

Single-income households are financially vulnerable now.

Especially in metro cities.

5. Lifestyle Inflation

Salary increases.

Expenses increase faster.

Savings remain zero.

That’s the trap.

Pro Tips to Reduce Monthly Expenses

- Cook more meals at home

- Avoid daily food delivery apps

- Use one credit card only

- Automate SIP investments

- Compare insurance yearly

- Review subscriptions quarterly

- Buy used furniture when possible

- Avoid unnecessary personal loans

Simple habits matter more than complicated budgeting apps.

Useful Financial Tools for Indian Families

Budget Tracking Apps

Investment Platforms

High-Interest Savings Accounts

Compare:

- SBI

- HDFC Bank

- ICICI Bank

- IDFC FIRST Bank

Small interest differences matter over years.

FAQ: Monthly Expense Breakdown for Middle-Class Families in India

How much does a middle-class family spend monthly in India?

Most families spend between ₹40,000 and ₹1 lakh monthly depending on city and lifestyle.

What percentage of salary should go to rent?

Keep rent below 30% of monthly income.

Higher than that creates financial pressure.

How much should Indian families save monthly?

Minimum 15–20% of income.

Even 10% is acceptable initially.

Consistency matters more.

Is ₹1 lakh salary enough for a family in India?

Yes, for most cities.

But lifestyle choices decide financial stability.

Not salary alone.

How much should be invested in SIPs monthly?

Start with ₹1,000–₹5,000 monthly.

Increase gradually after building emergency savings.

Which is the biggest expense for Indian families?

Usually:

- Rent

- Education

- Groceries

These three consume most income.

Conclusion

A proper monthly expense breakdown for middle-class families in India is not about living cheaply.

It is about avoiding financial stupidity.

Most families don’t fail because income is low.

They fail because spending is uncontrolled.

Track expenses.

Limit unnecessary EMIs.

Build emergency savings.

Invest monthly.

That alone puts you ahead of most people financially.