If you want to save tax under Section 80C, you’ll probably compare ELSS and PPF first. Both help reduce taxable income. But they work very differently.

Here’s the short answer:

- Choose ELSS if you want higher long-term returns.

- Choose PPF if you want guaranteed and safe returns.

- ELSS has a 3-year lock-in.

- PPF locks your money for 15 years.

- Many salaried Indians should actually use both.

This guide explains which one fits your income, risk level, and financial goals.

What Is ELSS and PPF?

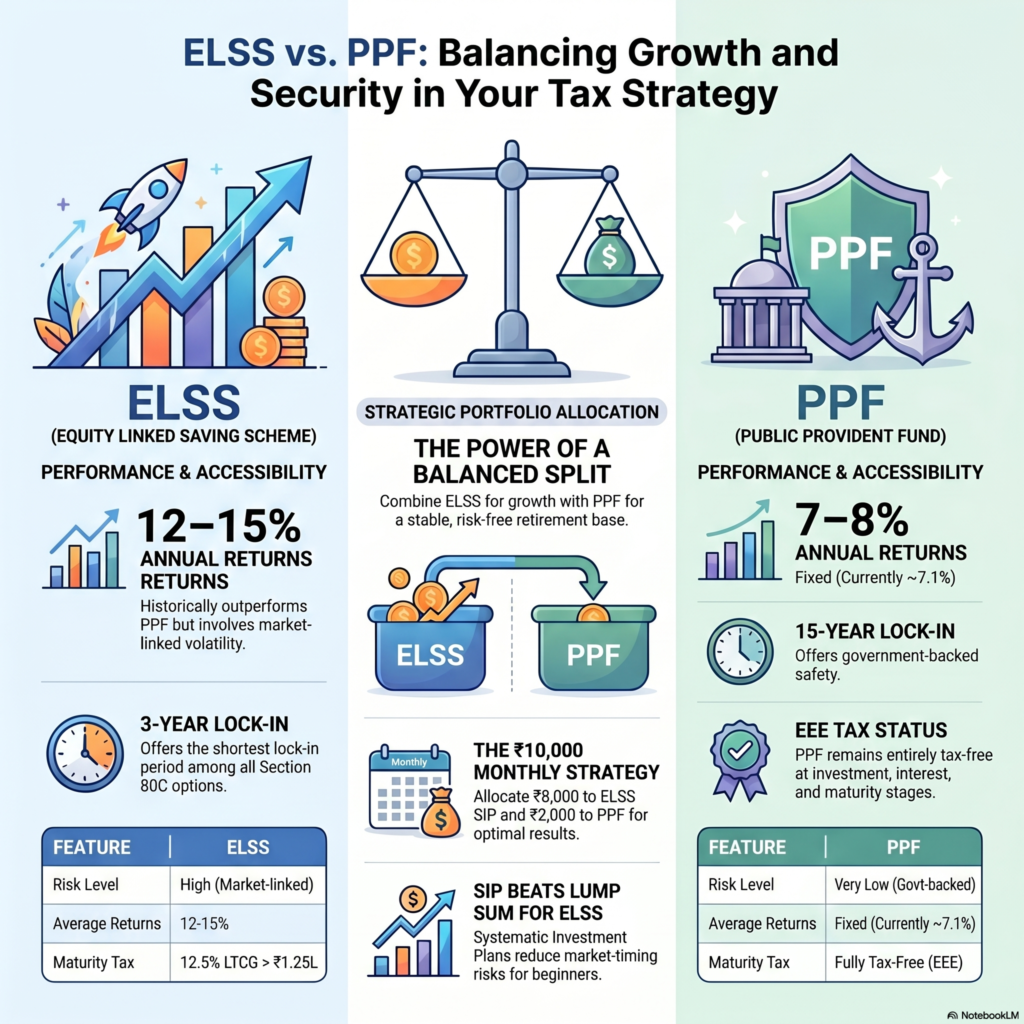

ELSS (Equity Linked Savings Scheme)

Equity Linked Savings Scheme is a tax-saving mutual fund.

It invests mostly in stocks. So returns are market-linked.

You can invest through SIP or lump sum.

Tax benefit comes under Section 80C up to ₹1.5 lakh yearly.

PPF (Public Provident Fund)

Public Provident Fund is a government-backed savings scheme.

Returns are fixed and decided by the government quarterly.

It is considered one of the safest investments in India.

You can open a PPF account in banks or post offices.

ELSS vs PPF: Quick Answer

| Feature | ELSS | PPF |

| Risk | High | Very Low |

| Returns | Market-linked | Fixed |

| Average Returns | 10–15% historically | Around 7–8% |

| Lock-in | 3 years | 15 years |

| Tax Benefit | Yes | Yes |

| Best For | Wealth creation | Safe savings |

| SIP Option | Yes | Yes |

| Inflation Beating | Better chance | Limited |

ELSS vs PPF: Which Gives Better Returns?

This is where most people make mistakes.

PPF feels safe. But safety alone does not build wealth.

ELSS Returns

ELSS funds invest in equity markets.

Good ELSS funds historically delivered around 12–15% annual returns over long periods.

But returns are not guaranteed.

Some years can be negative.

Example

₹5,000 monthly SIP for 15 years:

- At 12% return = around ₹25 lakh

- At 7% return = around ₹15 lakh

That difference matters.

PPF Returns

PPF interest is government-backed.

Current rates usually stay around 7–8%.

Returns are stable.

But inflation reduces real growth.

If inflation stays near 6%, your real return becomes very small.

ELSS vs PPF: Lock-In Period Comparison

ELSS Lock-In

Each ELSS investment stays locked for 3 years only.

This is the shortest tax-saving lock-in under Section 80C.

Good for people wanting flexibility.

PPF Lock-In

PPF locks your account for 15 years.

Partial withdrawal is allowed later.

But full flexibility is poor.

This becomes a problem for people needing liquidity.

ELSS vs PPF: Tax Benefits Explained

Both qualify under Section 80C.

Maximum deduction is ₹1.5 lakh yearly.

But taxation differs later.

| Tax Area | ELSS | PPF |

| Investment Deduction | Yes | Yes |

| Returns Taxed? | LTCG after limit | No |

| Maturity Tax | Partially taxable | Fully tax-free |

ELSS Taxation

Long-term capital gains above ₹1.25 lakh yearly are taxable.

Current LTCG tax on equity is 12.5%.

PPF Taxation

PPF is fully tax-free.

Investment, interest, and maturity are exempt.

This is called EEE taxation.

ELSS vs PPF: Risk Comparison

ELSS Risk

ELSS depends on stock market performance.

Short-term volatility is normal.

If markets crash, your portfolio can fall.

People panic and exit early. That destroys returns.

PPF Risk

PPF has almost zero default risk.

Returns are predictable.

Ideal for conservative investors.

But low risk usually means lower growth.

Who Should Choose ELSS?

Choose ELSS if:

- You are below 45 and building wealth

- You can stay invested 7–10 years

- You already have emergency savings

- You can handle market fluctuations

- You want inflation-beating returns

ELSS works better for long-term goals like:

- Retirement

- Child education

- Wealth creation

Who Should Choose PPF?

Choose PPF if:

- You hate market risk

- You want guaranteed returns

- You need stable retirement savings

- You are self-employed with irregular income

- You already invest in equities elsewhere

PPF works well for:

- Conservative investors

- Long-term debt allocation

- Safe retirement corpus

ELSS vs PPF for Salaried Employees

Most salaried people should not blindly choose one.

They should combine both.

Practical Split Example

Monthly salary: ₹50,000

Suggested 80C approach:

| Investment | Monthly Amount |

| EPF | ₹4,000 |

| ELSS SIP | ₹5,000 |

| PPF | ₹2,000 |

Why this works:

- EPF gives stability

- ELSS gives growth

- PPF gives safety

This creates balance instead of overdependence.

Real-Life Example: Chennai IT Employee

Rahul earns ₹8 lakh yearly in Chennai.

His monthly expenses:

| Expense | Amount |

| Rent | ₹15,000 |

| Groceries | ₹7,000 |

| Bike EMI | ₹4,500 |

| UPI spending | ₹8,000 |

| Savings | ₹10,000 |

He wants tax savings and future wealth.

Bad Decision

Putting entire ₹1.5 lakh into PPF.

Problem:

- Low liquidity

- Slower wealth growth

- Inflation impact

Better Decision

- ₹8,000 monthly in ELSS SIP

- ₹3,000 monthly in PPF

Result:

- Tax saving continues

- Wealth grows faster

- Some stability remains

That’s more practical.

Common Mistakes People Make

1. Choosing Only Based on Tax Saving

Tax saving alone is not investing.

Your goal matters more.

2. Expecting Guaranteed Returns From ELSS

Markets do not move upward every month.

Short-term volatility is normal.

3. Ignoring Inflation

A “safe” return may still lose purchasing power.

4. Locking Too Much Money in PPF

Many people regret liquidity issues later.

5. Stopping ELSS SIP During Market Crash

That usually hurts long-term returns badly.

Pro Tips Before Investing

Start ELSS SIP Instead of Lump Sum

SIP reduces timing risk.

Better for beginners.

Use PPF for Stability

Think of PPF as your safe bucket.

Not your wealth engine.

Don’t Invest Just Before March

People panic-invest for tax saving.

That leads to poor choices.

Review ELSS Funds Every Year

Not all funds perform consistently.

Keep Emergency Fund Separate

Never use ELSS or PPF as emergency money.

Best Platforms to Invest in ELSS and PPF

You can start ELSS SIPs using:

You can open PPF accounts through:

ELSS vs PPF: Pros and Cons

| Investment | Pros | Cons |

| ELSS | Higher return potential, short lock-in | Market risk |

| PPF | Safe, tax-free, stable | Long lock-in, lower growth |

FAQ

Is ELSS better than PPF?

For long-term wealth creation, usually yes.

For safety and guaranteed returns, no.

Depends on your goal.

Can I invest in both ELSS and PPF?

Yes.

Many investors should.

Both together create balance.

Which is safer: ELSS or PPF?

PPF is far safer.

ELSS depends on stock market performance.

Is ELSS fully tax-free?

No.

LTCG above ₹1.25 lakh yearly is taxable.

Can I withdraw PPF anytime?

No.

PPF has a 15-year maturity period.

Partial withdrawals have restrictions.

Which is best for beginners?

Risk-averse beginners may prefer PPF first.

Long-term investors should seriously consider ELSS SIPs.

Conclusion

The ELSS vs PPF debate is not really about “best.”

It’s about fit.

If you want higher growth and can tolerate market swings, ELSS is stronger long term.

If you want safety and guaranteed returns, PPF works better.

Most middle-class Indians should stop treating investing like a one-option decision.

A balanced mix usually works better than extremes.