Most Indians buy insurance the wrong way.

Someone from Life Insurance Corporation of India comes home.

They pitch a “safe” plan. You sign without thinking.

Years later, you realise:

- Cover is too low

- Returns are poor

- Family is still at risk

This article cuts through that confusion.

You’ll learn the real difference between term insurance vs LIC policies, and what actually works in India.

Quick Answer

- Term insurance gives high cover at low cost

- LIC policies mix insurance + savings (low returns)

- If your goal is protection → choose term insurance

- If your goal is forced savings → LIC plans may fit

- Best strategy: Buy term + invest separately

Insurance has one job: protect your family if you die.

That’s it.

But in India, many policies mix insurance with investment.

That’s where confusion starts.

Term insurance is pure protection.

LIC policies are usually combination products.

Understanding this difference will save you lakhs.

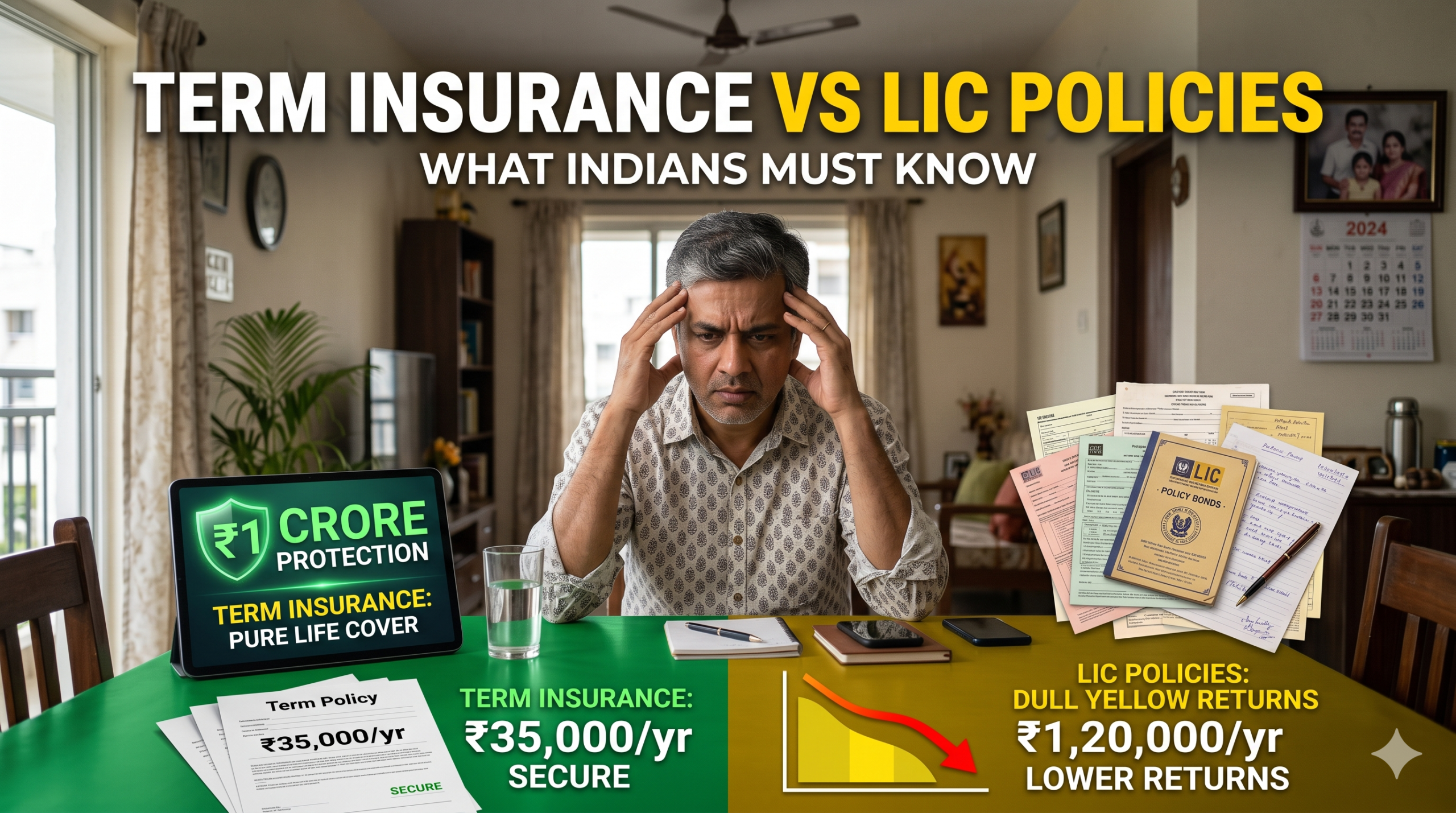

Term Insurance vs LIC Policies (Detailed Comparison)

Key Differences

| Feature | Term Insurance | LIC Policies |

| Purpose | Pure protection | Insurance + savings |

| Premium | Very low | High |

| Coverage | Very high (₹50L–₹2Cr) | Low (₹5L–₹20L typical) |

| Returns | None | Low (4–6% approx) |

| Flexibility | High | Low |

| Transparency | Simple | Complex |

Term Insurance: What, Why, Who

What it is

You pay a small premium for a large cover.

Why it works

You get maximum protection at minimum cost.

Who should use it

- Salaried employees

- Family breadwinners

- Anyone with dependents

Example

₹800/month can give ₹1 crore cover.

That’s serious protection.

LIC Policies: What, Why, Who

What it is

Plans like endowment, money-back, ULIPs.

Why people buy it

- Guaranteed feeling

- Forced savings

- Trust in LIC brand

Who should use it

- People who struggle to save

- Extremely risk-averse investors

Reality check

Returns often barely beat inflation.

Pros and Cons

Term Insurance

Pros

- Cheap

- High coverage

- Simple to understand

Cons

- No maturity benefit

- Requires discipline to invest separately

LIC Policies

Pros

- Forced savings

- Low perceived risk

- Some guaranteed returns

Cons

- Low coverage

- Poor returns

- Complex structure

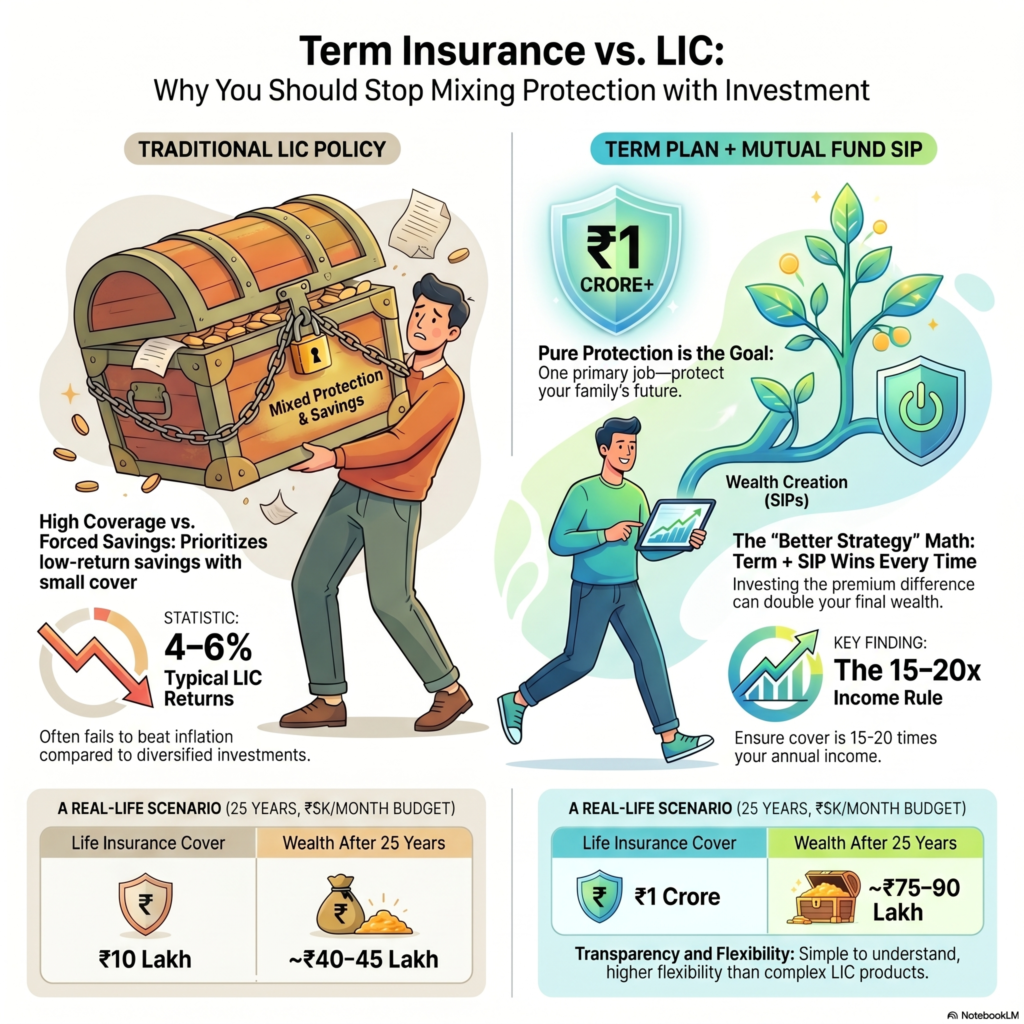

Real-Life Example

Rahul earns ₹40,000/month in Chennai.

Option 1: LIC Policy

- Premium: ₹5,000/month

- Cover: ₹10 lakh

- Return: ~5%

Option 2: Term + Investment

- Term plan: ₹1,000/month for ₹1 crore cover

- Invest ₹4,000 in SIP (12% return)

After 25 years:

- LIC corpus: ~₹40–45 lakh

- SIP corpus: ~₹75–90 lakh

And Rahul still had ₹1 crore protection all along.

This isn’t close. It’s obvious.

Common Mistakes Indians Make

- Mixing insurance with investment

- Buying policies just for tax saving

- Underestimating required coverage

- Trusting agents blindly

- Ignoring inflation

These mistakes cost decades of money.

Pro Tips (Actionable)

- Take cover = 15–20x your annual income

- Choose online term plans (cheaper)

- Avoid “guaranteed return” traps

- Increase cover after marriage or kids

- Review policy every 5 years

Tools & Platforms

If you’re serious:

- Compare term plans on Policybazaar

- Check claim settlement ratios on Insurance Regulatory and Development Authority of India

- Start SIPs via Groww or Zerodha Coin

Don’t overthink. Just separate insurance and investing.

FAQ (SEO Boost)

1. Is term insurance better than LIC?

For protection, yes. It gives higher coverage at lower cost.

2. Why do people still buy LIC policies?

Trust, simplicity, and forced savings habit.

3. Can I have both term insurance and LIC policy?

Yes. But don’t rely on LIC for protection.

4. What is ideal term insurance coverage?

At least 15–20 times your yearly income.

5. Are LIC returns good?

Usually 4–6%. Often below inflation-adjusted needs.

6. Is term insurance safe in India?

Yes, if you choose a reputed insurer with good claim history.

Conclusion

Stop mixing two different goals.

Insurance is for protection.

Investment is for wealth.

Term insurance vs LIC policies is not a close fight.

One protects your family properly. The other dilutes both goals.

Buy a term plan.

Invest the rest.

That’s the simplest strategy that actually works in India.