Confused between a savings account and a current account?

You’re not alone.

Many people open the wrong account and lose money in fees.

Or worse, they limit their business growth without knowing it.

In this guide, you’ll learn the exact difference, when to use each, and what actually makes sense in India.

QUICK ANSWER

Savings Account vs Current Account (India):

- Savings account → Best for individuals to save money and earn interest

- Current account → Best for businesses with frequent transactions

- Savings accounts have withdrawal limits but earn interest

- Current accounts have no limits but usually no interest

- Choose based on usage, not just convenience

Banks offer different accounts for different needs.

Savings accounts are built for personal money management.

Current accounts are built for business transactions.

Using the wrong one leads to penalties, low returns, or blocked transactions.

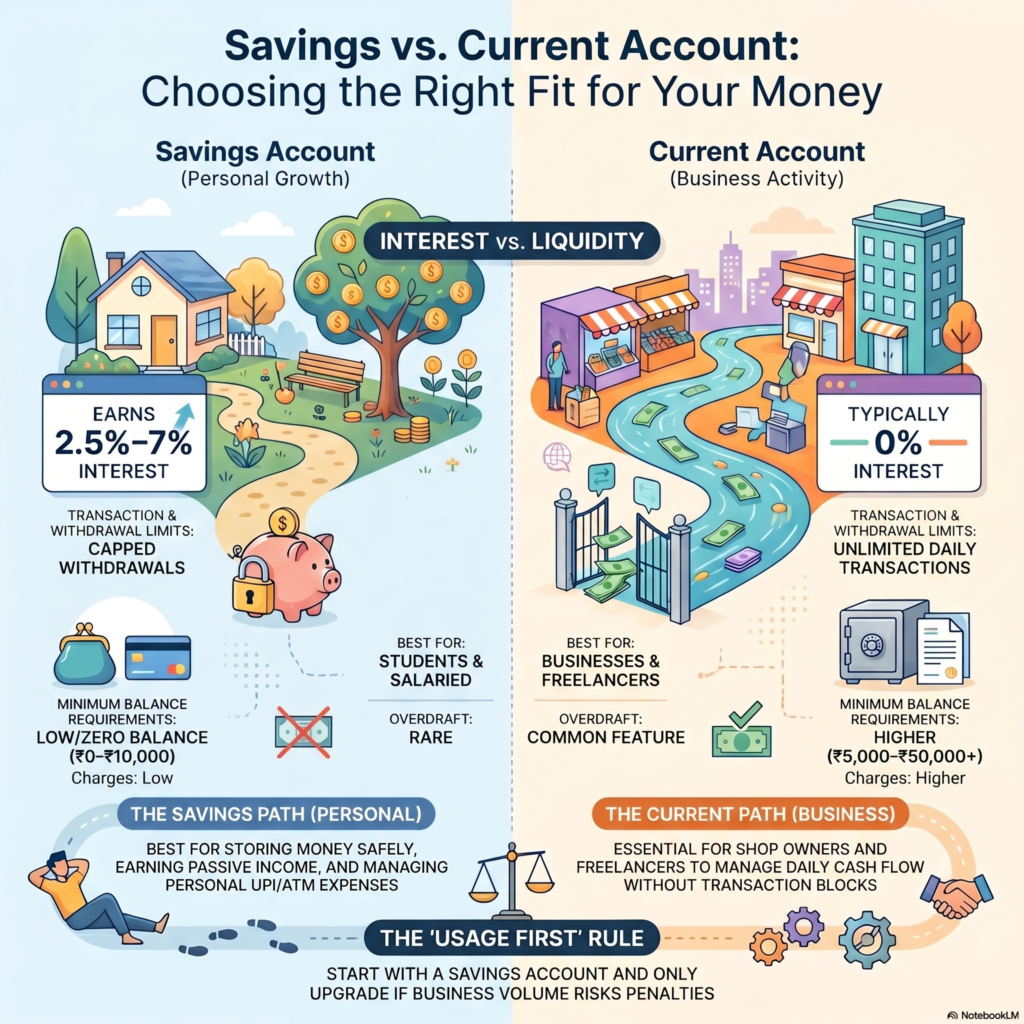

SAVINGS ACCOUNT VS CURRENT ACCOUNT (FULL COMPARISON)

| Feature | Savings Account | Current Account |

| Purpose | Personal savings | Business transactions |

| Interest | 2.5%–7% per year | Usually 0% |

| Transaction Limit | Limited | Unlimited |

| Minimum Balance | Low or zero (₹0–₹10,000) | Higher (₹5,000–₹50,000+) |

| Best For | Salaried, students | Businesses, freelancers |

| Overdraft | Rare | Common feature |

| Charges | Low | Higher |

WHAT IS A SAVINGS ACCOUNT?

What it is

A basic account to store your money safely and earn interest.

Why it works

You earn passive income on your balance.

Also supports UPI, ATM, and online payments.

Who should use it

- Salaried employees

- Students

- Beginners in finance

Example

You keep ₹50,000 in your account.

At 3% interest, you earn ~₹1,500 yearly without effort.

Action

Open a zero-balance savings account if starting fresh.

WHAT IS A CURRENT ACCOUNT?

What it is

An account designed for high-volume transactions.

Why it works

No limits on deposits or withdrawals.

Helps manage daily business cash flow.

Who should use it

- Shop owners

- Freelancers with regular payments

- Small business owners

Example

You run a shop and handle ₹2 lakh monthly transactions.

A savings account will restrict you.

A current account won’t.

Action

Open a current account if you handle frequent payments daily.

REAL-LIFE EXAMPLE

Ravi earns ₹30,000 per month.

- Rent: ₹8,000

- Groceries: ₹6,000

- UPI payments: ₹5,000

- Savings: ₹5,000

He uses a savings account.

He earns small interest and manages expenses easily.

Now consider Priya.

She runs a boutique.

- Monthly sales: ₹2.5 lakh

- Vendor payments: ₹1.5 lakh

- Daily UPI + bank transfers

She needs a current account.

Otherwise, her transactions may get blocked or penalized.

COMMON MISTAKES

- Using a savings account for business transactions

- Ignoring minimum balance rules

- Opening current account without actual need

- Choosing account based only on “zero balance” ads

- Not checking hidden charges and fees

PRO TIPS

- Start with savings account. Upgrade only if needed

- Compare banks. Don’t pick randomly

- Check ATM, SMS, and maintenance charges

- Use one account for expenses, one for savings

- Enable UPI and auto-pay to simplify payments

SMART NEXT STEP

If you’re just starting, open a savings account with banks like:

- HDFC Bank (good app + reliability)

- ICICI Bank (strong digital features)

- SBI (low cost, wide network)

If you run a business, explore current accounts with:

- ICICI or HDFC for smoother transactions

- Axis Bank for startup-friendly options

Also consider linking your account with SIP apps or investment platforms to grow money automatically.

FAQ SECTION

1. Can I use a savings account for business?

You can, but it’s not ideal.

Banks may flag or restrict heavy transactions.

2. Do current accounts give interest?

No, most current accounts do not offer interest.

3. Which account is better for salary?

Savings account. It’s built for personal income and expenses.

4. What is minimum balance in current account?

Usually ₹5,000 to ₹50,000 depending on the bank.

5. Can I have both accounts?

Yes. Many people use both for better money management.

6. Is zero balance account good?

Yes for beginners. But check for hidden charges.

CONCLUSION

The choice is simple.

If you earn and spend personally, go for a savings account.

If you handle frequent business transactions, choose a current account.

Don’t overcomplicate it.

Match the account to your usage, not what others are doing.

That’s how you avoid fees and manage money better.