Most Indians don’t have an income problem first.

They have a money discipline problem.

Salary comes in. UPI spending starts. Swiggy, EMI, shopping, subscriptions, random “small” expenses. By the 20th, bank balance looks weak again.

That cycle keeps repeating for years.

The good news? Financial discipline is not about being cheap. It’s about controlling your money before it controls you.

In this guide, you’ll learn how to build discipline with money in an Indian lifestyle using practical methods that actually work.

Quick Answer: How to Build Discipline With Money

- Track every expense for 30 days

- Separate spending and savings accounts

- Automate SIPs immediately after salary credit

- Use UPI with daily limits

- Follow a fixed “fun money” budget monthly

Small systems work better than motivation.

What Financial Discipline Actually Means

Financial discipline means using money intentionally.

Not emotionally.

You don’t buy things because you are bored, stressed, or influenced online. You spend according to priorities.

A disciplined person can still enjoy life.

They simply avoid stupid financial habits repeatedly.

That difference matters.

Step-by-Step: How to Build Discipline With Money in India

1. Know Where Your Money Is Going

Most people underestimate spending badly.

Especially UPI payments.

₹120 here. ₹250 there. Daily tea, snacks, quick online orders. It looks harmless individually.

But together, it destroys savings.

What to do

Track every expense for one month.

Use apps like:

- CRED

- Walnut

- Money View

Or use Google Sheets.

Example

If you earn ₹35,000:

- Food delivery: ₹4,500

- Random UPI spends: ₹3,000

- OTT subscriptions: ₹1,200

- Impulse shopping: ₹2,500

That’s ₹11,200 leaking monthly.

You cannot fix what you don’t measure.

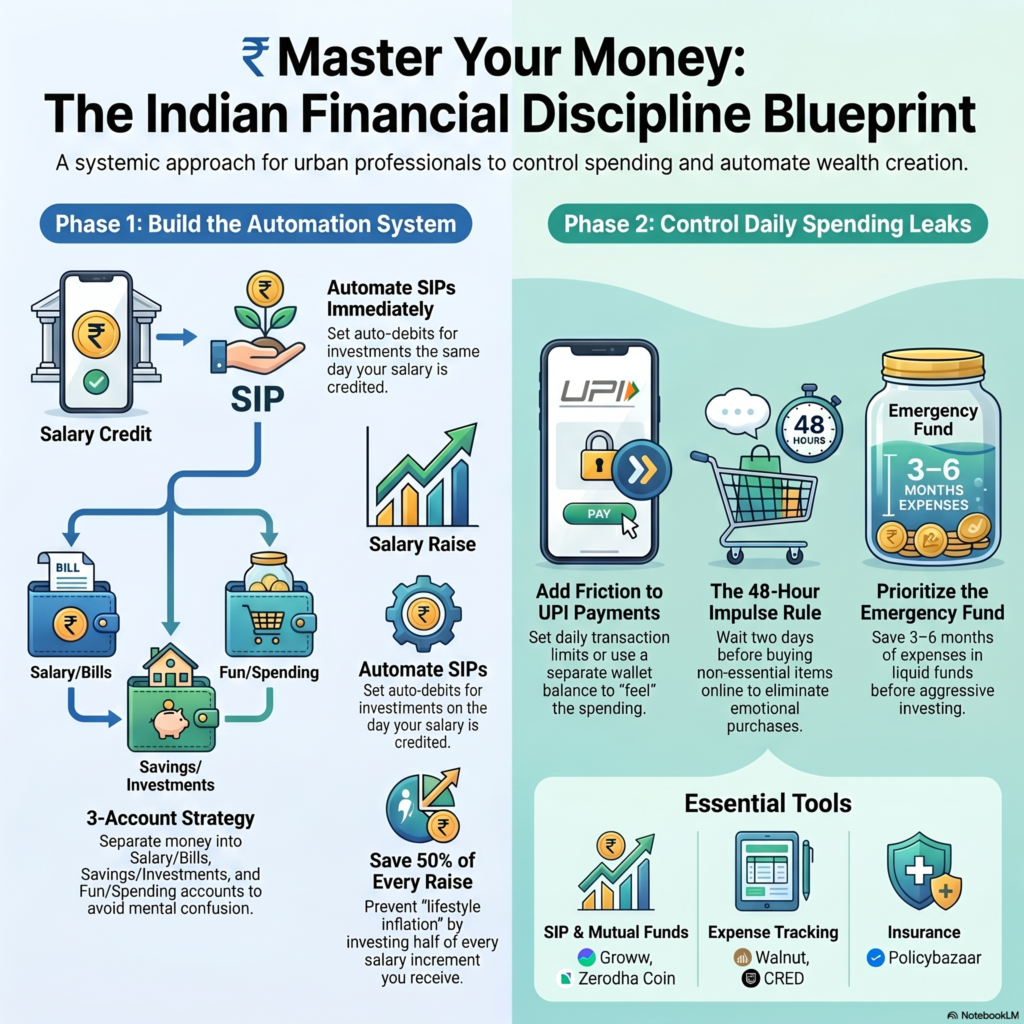

2. Automate Savings Before Spending

This is the biggest discipline hack.

Do not “save whatever is left.”

Nothing will be left.

What to do

The moment salary comes:

- Move savings automatically

- Start SIP auto-debits

- Transfer emergency fund money

Example

Salary: ₹40,000

Immediately:

- ₹5,000 SIP

- ₹3,000 emergency fund

- ₹2,000 insurance/investment

Now your usable money becomes ₹30,000.

That forces discipline naturally.

Best tools

3. Use Separate Bank Accounts

This works surprisingly well.

When salary and spending happen in one account, you lose clarity.

Better system

Use:

- Account 1 = Salary + bills

- Account 2 = Savings/investing

- Account 3 = Spending/fun money

Why it works

Your brain behaves differently when money is separated.

You stop mentally counting savings as spendable cash.

Good banking options

4. Control UPI Spending

UPI made payments easy.

Too easy.

You no longer “feel” spending.

That creates careless habits.

How to build discipline with money using UPI controls

Do this

- Set daily transaction limits

- Remove saved cards from shopping apps

- Disable one-click payments

- Use wallet balance instead of bank balance

Practical trick

Keep only weekly spending money in your UPI-linked account.

If the account empties early, spending stops automatically.

Simple.

5. Create Rules for Impulse Buying

Discipline is easier with rules.

Not decisions.

Good money rules

- Wait 48 hours before buying online

- No EMI for gadgets

- No shopping during salary week

- Uninstall shopping apps during weekdays

These sound small.

But they reduce emotional spending massively.

6. Build an Emergency Fund First

People ignore this.

Then one medical issue or job loss destroys finances.

Without emergency savings, discipline collapses fast.

Minimum target

Save:

- 3 months expenses initially

- 6 months eventually

Example

Monthly expenses = ₹25,000

Emergency fund target:

- Minimum: ₹75,000

- Better: ₹1.5 lakh

Keep this in:

- High-interest savings account

- Liquid mutual fund

- FD

Not stocks.

7. Stop Lifestyle Inflation Early

Every salary hike creates new expenses.

Better phone. Bigger bike EMI. Expensive weekends.

That’s how people earning ₹1 lakh still stay broke.

Smarter rule

Whenever salary increases:

- Save at least 50% of the increment

Example

Salary increased by ₹10,000.

Do this:

- Invest ₹5,000

- Spend ₹5,000

Not ₹10,000 spending.

8. Use Cash for Weak Areas

Digital money hides pain.

Cash exposes it.

If you overspend on:

- Food delivery

- Snacks

- Shopping

- Weekend outings

Use physical cash weekly.

Why this works

Handing over ₹500 feels different than tapping UPI.

Behavior changes immediately.

Real-Life Indian Example

Rahul, Age 29, Chennai

Monthly salary: ₹45,000

Before discipline

- Rent: ₹12,000

- Food delivery: ₹5,500

- Bike EMI: ₹4,000

- Random UPI spends: ₹6,000

- Shopping: ₹4,500

- Savings: ₹2,000

End-of-month stress every time.

After discipline system

- SIP auto-investment: ₹6,000

- Emergency fund: ₹3,000

- UPI weekly limit: ₹2,500

- Food budget fixed: ₹3,000

- Shopping wait rule: 48 hours

Savings increased to ₹12,000 monthly within 5 months.

Income didn’t change.

Behavior changed.

Common Mistakes People Make

1. Depending on motivation

Motivation disappears quickly.

Systems stay.

2. Using credit cards for lifestyle

Credit cards are tools.

Not extra income.

3. Ignoring subscriptions

Small recurring charges quietly drain money.

Audit monthly.

4. Taking unnecessary EMIs

Most EMIs reduce future freedom.

Especially for gadgets.

5. Investing before controlling spending

Bad money habits will eventually destroy investing discipline too.

Pro Tips to Build Financial Discipline Faster

- Increase SIP yearly automatically

- Keep savings in another bank

- Avoid checking shopping apps daily

- Use expense alerts from banking apps

- Review expenses every Sunday for 10 minutes

Consistency matters more than intensity.

Useful Financial Tools for Indians

These tools can help automate discipline:

| Purpose | Recommended Platform |

| SIP Investing | Groww |

| Direct Mutual Funds | Zerodha Coin |

| Expense Tracking | Walnut |

| Credit Score Tracking | CIBIL |

| Insurance Comparison | Policybazaar |

Don’t use ten apps.

Use two or three consistently.

FAQs

How long does it take to build money discipline?

Usually 3–6 months of consistent habits.

Not 7 days.

What is the best way to control unnecessary spending?

Track expenses and limit UPI access.

Awareness changes behavior fast.

Should I stop enjoying life to save money?

No.

You need controlled spending, not miserable living.

Is budgeting enough for financial discipline?

No.

Automation and spending control matter more.

How much should Indians save monthly?

At least 20% initially.

More if income increases.

Are SIPs good for disciplined investing?

Yes.

Automatic SIPs remove emotional investing decisions.

Conclusion

Learning how to build discipline with money is mostly behavioral.

Not mathematical.

Most people already know basic finance advice.

The problem is inconsistent execution.

Track spending.

Automate savings.

Control UPI leakage.

Avoid emotional purchases.

That’s the real foundation of financial discipline in India.

Do boring money habits consistently for two years.

Your financial life will look completely different.