One unexpected expense can break your entire budget.

Hospital bill. Job loss. Family emergency.

Most people in India don’t have backup money. They rely on credit cards or loans. That’s expensive and risky.

So how much emergency fund do you actually need?

Not theory. Not “6 months blindly.”

Let’s break it down with real Indian numbers and a simple method.

QUICK ANSWER

How much emergency fund you need in India:

- Minimum: 3 months of essential expenses

- Safe level: 6 months of essential expenses

- Risky job / freelancer: 9–12 months

- Dual income family: 3–4 months may be enough

- Always calculate based on expenses, not salary

An emergency fund is money you keep aside for unexpected situations.

Not for vacations. Not for gadgets.

Only for:

- Job loss

- Medical emergencies

- Urgent home repairs

This money must be:

- Easy to access

- Safe (no risk)

- Separate from your main account

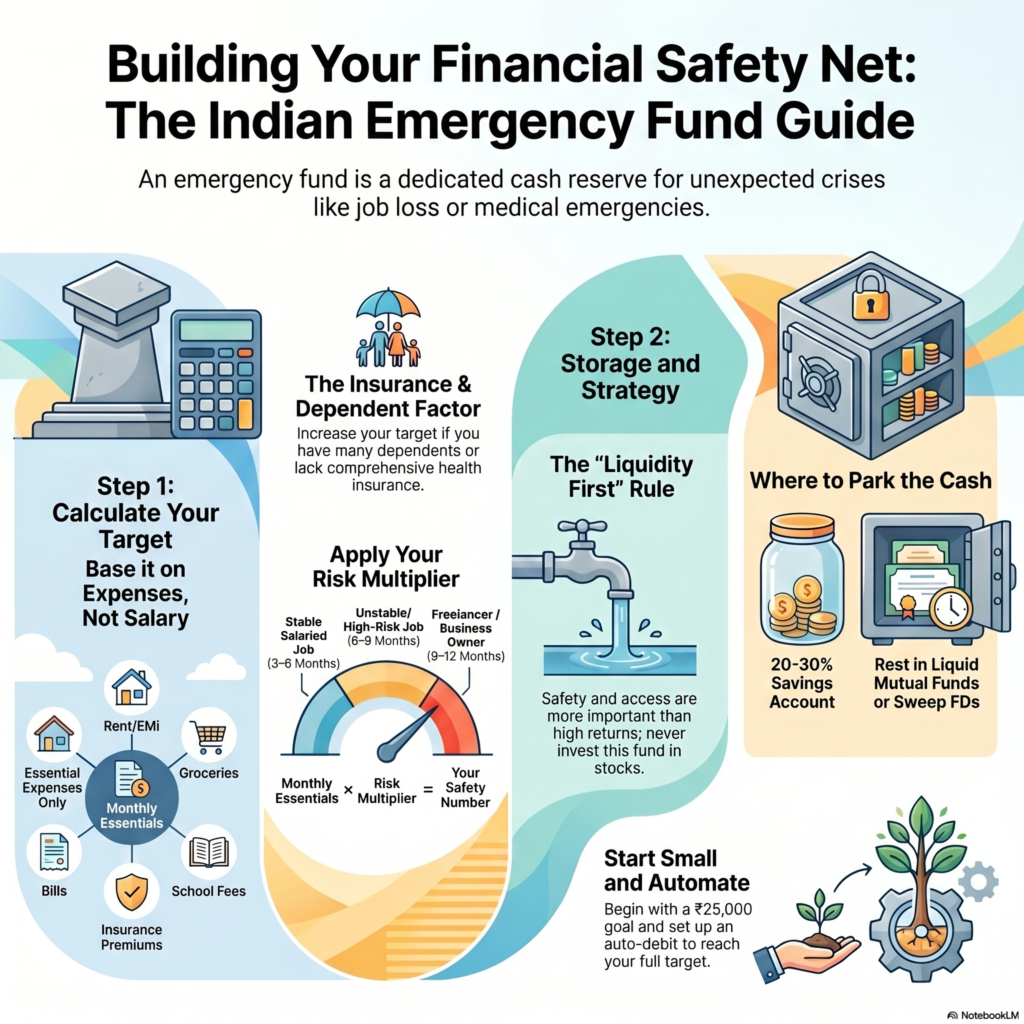

HOW TO CALCULATE YOUR EMERGENCY FUND (STEP-BY-STEP)

Step 1: Calculate Essential Monthly Expenses

Don’t include luxuries.

Only count what you must pay to survive.

Include:

- Rent / EMI

- Groceries

- Electricity + mobile bills

- School fees

- Basic transport

- Insurance premiums

Example:

- Rent: ₹12,000

- Groceries: ₹8,000

- Bills: ₹3,000

- Transport: ₹2,000

- Insurance: ₹2,000

Total = ₹27,000

Action: Write your actual monthly essentials.

Step 2: Multiply by Risk Level

Now choose based on your situation:

- Stable job → × 3 to 6

- Unstable job → × 6 to 9

- Freelancer/business → × 9 to 12

Example:

₹27,000 × 6 = ₹1,62,000

Action: Pick a number that matches your job stability.

Step 3: Adjust for Dependents

More dependents = higher risk.

- Single → lower fund

- Married → moderate

- Kids + parents → higher fund

Example:

If family depends on you → aim for 6–9 months minimum.

Action: Increase your fund if others depend on your income.

Step 4: Factor Insurance (Critical Shortcut)

If you have:

- Health insurance

- Term insurance

Your emergency fund burden reduces.

Without insurance, your emergency fund must be higher.

Action: If uninsured, increase target by at least 2–3 months.

Step 5: Decide Where to Keep It

Don’t invest emergency money in risky assets.

Use:

- Savings account

- Liquid mutual funds

- Sweep FD

Rule: Liquidity > returns

REAL-LIFE EXAMPLE (INDIAN SCENARIO)

Rahul works in Chennai. Salary: ₹45,000.

Monthly essentials:

- Rent: ₹10,000

- Food: ₹7,000

- Bills: ₹3,000

- Transport: ₹2,500

- Insurance: ₹2,500

Total: ₹25,000

He has a stable job.

So he chooses 6 months.

Emergency fund = ₹25,000 × 6 = ₹1,50,000

He builds it slowly:

- Saves ₹10,000/month

- Reaches goal in 15 months

No stress. No loans.

COMMON MISTAKES

1. Using salary instead of expenses

Wrong base. You inflate your target unnecessarily.

2. Investing emergency fund in stocks

Market crash + emergency = disaster.

3. Keeping everything in one account

Easy to spend accidentally.

4. Ignoring insurance

One hospital bill can wipe out savings.

5. Waiting to “start later”

Emergencies don’t wait for your plan.

PRO TIPS

- Start with ₹25,000. Don’t wait for perfect amount

- Automate savings monthly

- Keep 20–30% in savings account, rest in liquid fund

- Increase fund when income increases

- Recalculate every year

TOOLS & PLATFORMS

To build your emergency fund faster, use:

- Auto-debit savings in your bank

- Liquid funds via platforms like Groww or Zerodha Coin

- High-interest savings accounts from banks like ICICI or HDFC

If you don’t have insurance yet, fix that first.

Emergency fund + insurance = real safety.

FAQ SECTION

1. Is 3 months emergency fund enough in India?

Yes, but only for very stable jobs. Otherwise, aim for 6 months.

2. Where should I keep my emergency fund?

Savings account + liquid mutual funds. Avoid stocks or crypto.

3. Can I use FD for emergency fund?

Yes, but use sweep-in FD for quick access.

4. Should I build emergency fund or invest first?

Emergency fund comes first. Investing comes after.

5. How long does it take to build an emergency fund?

Depends on savings rate. Usually 6–18 months.

6. What if I have debt?

Build a small emergency fund (₹25k–₹50k), then focus on debt.

CONCLUSION

Your emergency fund is not a random number.

It’s based on your expenses, job risk, and responsibilities.

For most people in India:

6 months of essential expenses is the sweet spot.

Start small. Stay consistent.

Because when things go wrong, this fund decides whether you panic… or stay in control.