You tried budgeting. Maybe the 50-30-20 rule.

And it failed.

Salary comes in. Rent eats half. Groceries rise. EMIs don’t wait. By the 20th, you’re broke.

That’s the reality for most Indians.

So the question is simple:

Is 50-30-20 even practical in India?

In this guide, you’ll see what actually works with Indian salaries. Not theory. Real numbers. Real fixes.

Quick Answer

Best budgeting method for Indian salaries:

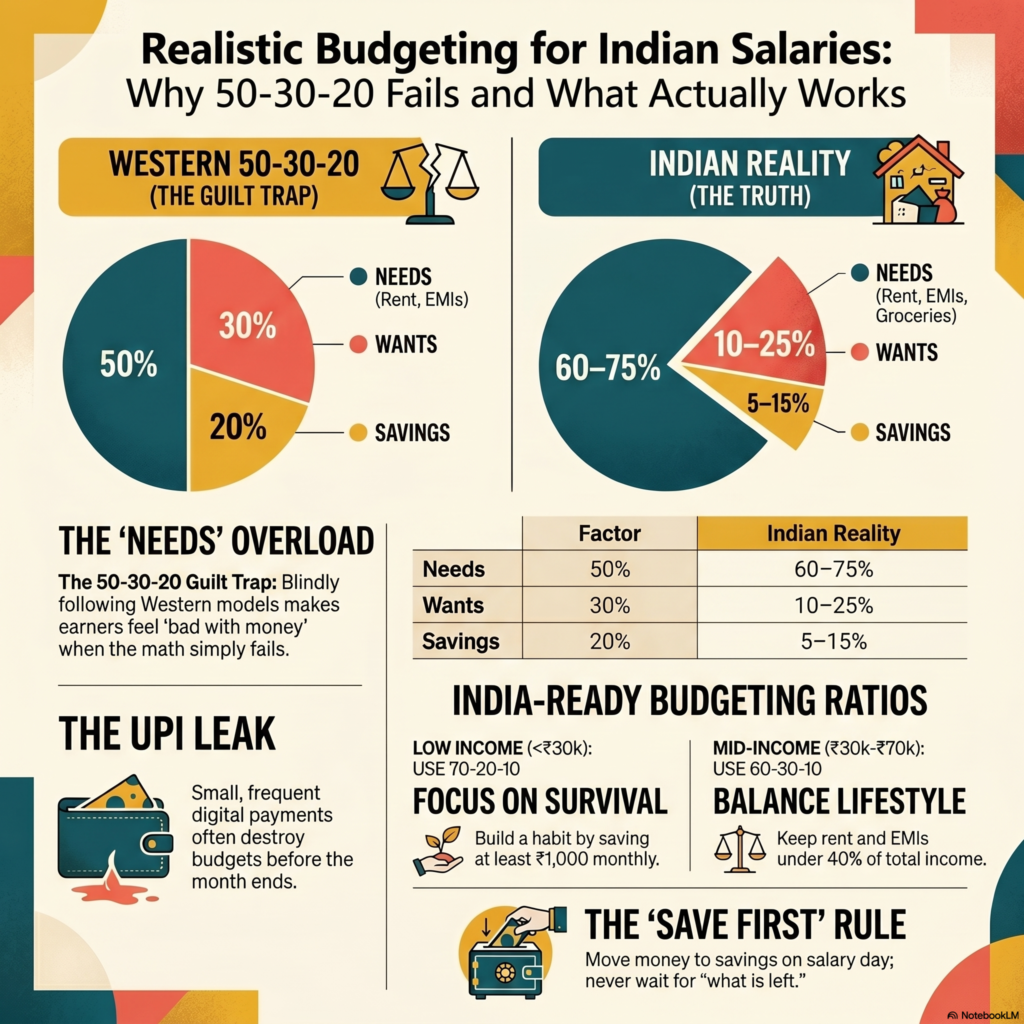

- Start with a 60-30-10 or 70-20-10 rule, not 50-30-20

- Fix savings first, even if small (₹1,000 minimum)

- Cut “wants” brutally, not softly

- Adjust ratios based on rent, EMI, and city

- Use UPI tracking apps to stay consistent

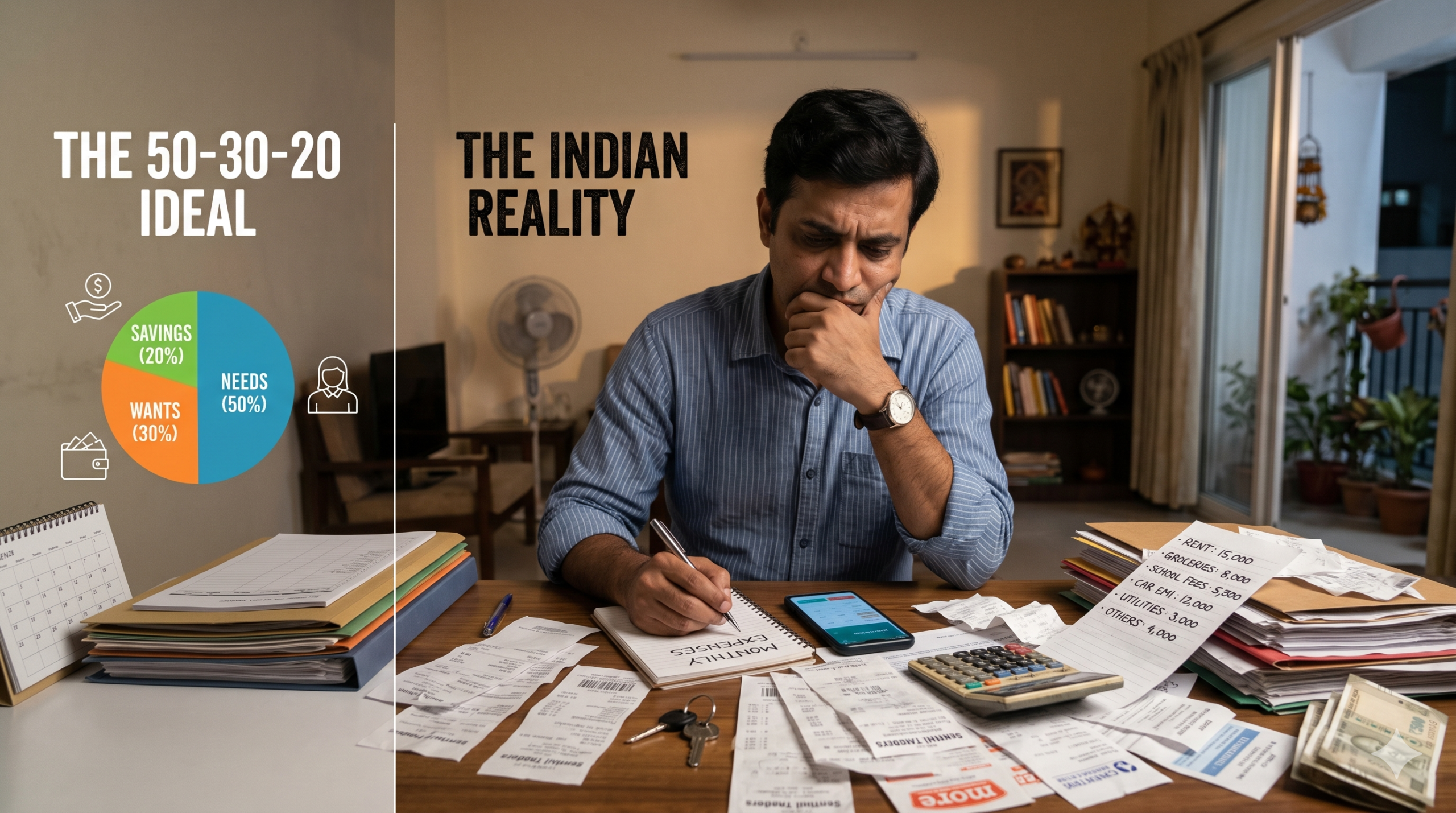

What is the 50-30-20 Rule?

Simple idea:

- 50% → Needs (rent, food, bills)

- 30% → Wants (shopping, eating out)

- 20% → Savings

Works well in Western countries.

But here’s the problem.

In India, needs alone can cross 60–70%.

So blindly following this rule is unrealistic.

50-30-20 vs Reality in India

Comparison Table

| Factor | 50-30-20 Rule | Indian Reality |

| Needs | 50% | 60–75% |

| Wants | 30% | 10–25% |

| Savings | 20% | 5–15% |

| Rent impact | Moderate | Very high |

| EMI burden | Low | Common |

| Practical? | Yes (abroad) | Rarely |

What this means

If you try 50-30-20 in India:

- You feel guilty for not saving 20%

- You think you’re “bad with money”

- But actually, the system doesn’t fit your income

Best Budgeting Method for Indian Salaries

1. Start with 70-20-10 (Low Income)

What it is:

- 70% needs

- 20% wants

- 10% savings

Why it works:

Matches real expenses.

Who should use it:

Salary below ₹30,000

Example:

₹25,000 salary

- Needs: ₹17,500

- Wants: ₹5,000

- Savings: ₹2,500

Action:

Start saving even ₹1,000. Build habit first.

2. Use 60-30-10 (Mid Income)

What it is:

- 60% needs

- 30% wants

- 10% savings

Why it works:

Balances lifestyle and control.

Who should use it:

₹30,000–₹70,000 salary

Action:

Cap rent + EMI under 40% total income.

3. Upgrade to 50-30-20 (Only When Ready)

What it is:

The original model.

Why it works:

High saving potential.

Who should use it:

Stable income + low debt

Action:

Don’t jump here early. Earn your way into it.

Real-Life Example (Indian Scenario)

Let’s take a ₹40,000 salary in Chennai.

Expenses Breakdown:

- Rent: ₹12,000

- Groceries: ₹5,000

- Transport: ₹3,000

- Utilities: ₹2,000

- EMI: ₹5,000

Total needs = ₹27,000 (67%)

Now reality hits.

You cannot fit this into 50%.

Practical Budget:

- Needs: ₹27,000

- Wants: ₹8,000

- Savings: ₹5,000

This is roughly 67-20-13

Not perfect. But sustainable.

Common Mistakes

1. Copy-pasting foreign advice

Indian costs are different. Stop blindly following YouTube rules.

2. Ignoring rent reality

If rent is 40%, your budget is already broken.

3. Saving “what’s left”

Nothing will be left. Save first.

4. Not tracking UPI spending

Small ₹200 payments destroy your budget.

5. Trying to be perfect

Consistency beats perfection.

Pro Tips That Actually Work

- Fix one saving rule: Save on salary day

- Use two accounts: spending + savings

- Track weekly, not monthly

- Cut subscriptions aggressively

- Increase income. Budgeting alone won’t save you

Tools to Make Budgeting Easier

You don’t need complicated systems.

Start simple:

- Expense tracking apps like Walnut or Money Manager

- SIP platforms for automatic investing

- UPI apps with transaction history

- Basic savings account with auto transfer

If you’re serious, automate:

- SIP for mutual funds

- Recurring deposit for discipline

- Health insurance (don’t skip this)

FAQs

Is 50-30-20 rule realistic in India?

No, not for most people. Expenses are higher relative to income.

What is the best budgeting rule for ₹30,000 salary?

Start with 70-20-10. Focus on survival and habit.

How much should I save monthly in India?

Minimum 10%. Even ₹1,000 is fine initially.

Should I invest or save first?

Save an emergency fund first. Then invest.

How to control unnecessary spending?

Track UPI expenses. That’s where money leaks.

Conclusion

The best budgeting method for Indian salaries is not 50-30-20.

It’s whatever you can actually follow every month.

Start with reality:

- High rent

- Fixed EMIs

- Rising costs

Then adjust:

- Save small

- Track spending

- Increase income

Don’t chase perfect ratios.

Build a system you won’t quit.