You need money fast. Medical bill, wedding, or credit card mess.

Personal loan looks easy. No collateral, quick approval.

But here’s the problem.

Most people take it without understanding the real cost.

This guide gives you the honest reality.

When a personal loan makes sense, and when it can trap you.

Quick Answer

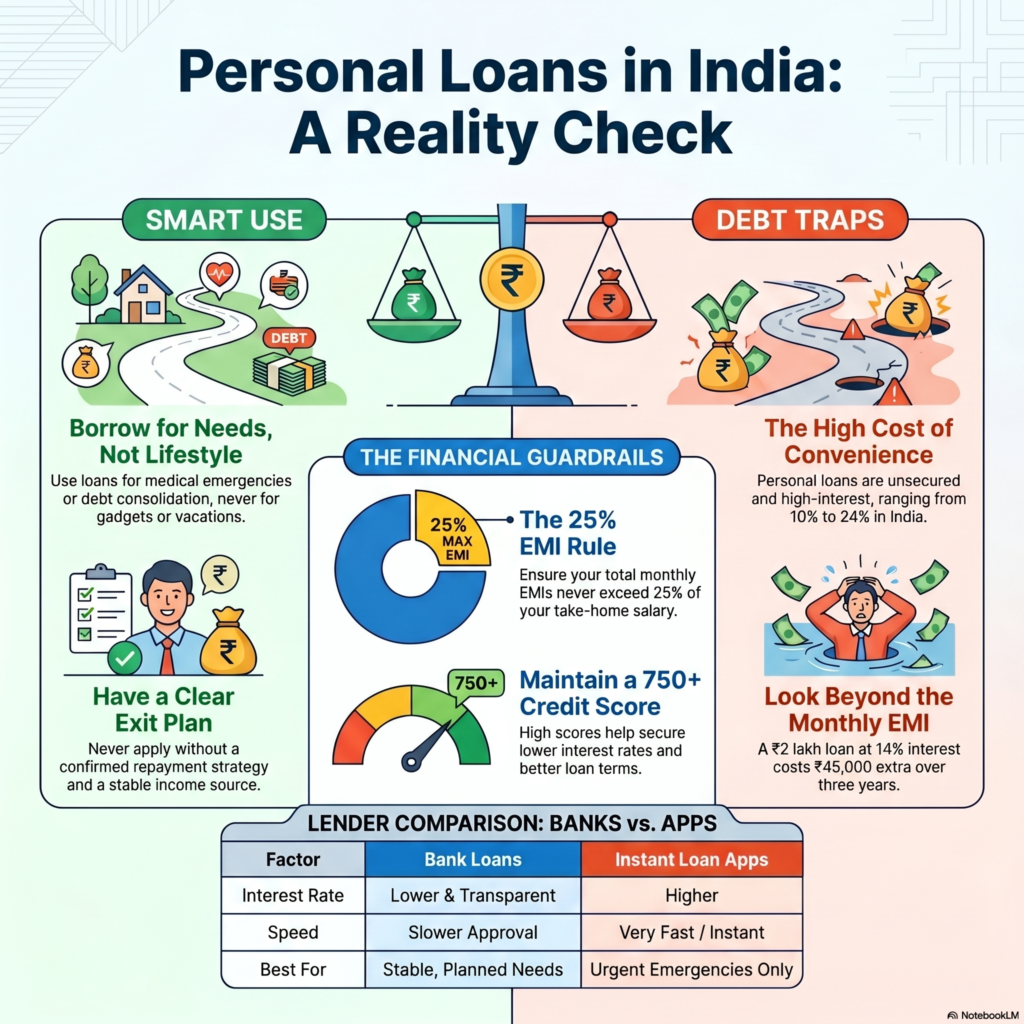

- Take a personal loan only for urgent or high-value needs

- Avoid it for lifestyle spending or impulse buying

- Check total interest, not just EMI

- Ensure EMI is below 20–25% of your income

- Have a clear repayment plan before applying

What Is a Personal Loan? (Simple Explanation)

A personal loan is unsecured. No collateral needed.

Banks and apps give it based on your income and credit score.

Interest rates are high. Usually 10% to 24% in India.

Tenure ranges from 1 to 5 years.

You get money quickly. But you pay heavily for that speed.

Should You Take a Personal Loan in India? (Full Breakdown)

1. When It Makes Sense

What it is: Borrowing for real needs, not wants

Why it works: Solves urgent problems without selling assets

Who should use it: Salaried people with stable income

Examples:

- Medical emergency

- Essential home repair

- High-interest debt consolidation

Action:

If the expense is unavoidable and urgent, consider it.

2. When It’s a Bad Idea

What it is: Borrowing for comfort or status

Why it fails: You pay interest for things that lose value

Who should avoid: Anyone with unstable income

Examples:

- Buying a phone on loan

- Funding a vacation

- Shopping during sales

Action:

If it’s not urgent, don’t borrow. Delay or save instead.

3. Real Cost of a Personal Loan (Most People Ignore This)

What it is: Total repayment, not EMI

Why it matters: EMI looks small, but interest adds up

Example:

Loan: ₹2,00,000

Interest: 14%

Tenure: 3 years

EMI: ~₹6,800

Total repayment: ~₹2,45,000

You pay ₹45,000 extra. That’s the real cost.

Action:

Always check total interest before taking a loan.

4. Income Check Rule (Non-Negotiable)

What it is: EMI vs income ratio

Why it matters: High EMI kills your monthly budget

Rule:

Your total EMIs should not exceed 25% of income

Example:

Salary: ₹30,000

Safe EMI: ₹7,500 max

Action:

If EMI crosses this, don’t take the loan.

5. Compare Before You Apply

| Factor | Bank Loan | Instant Loan Apps |

| Interest | Lower | Higher |

| Approval | Slower | Very fast |

| Charges | Transparent | Often hidden |

| Best for | Stable income | Emergency only |

Action:

Start with banks. Use apps only if urgent.

Real-Life Example

Ravi earns ₹35,000 per month in Chennai.

Expenses:

- Rent: ₹10,000

- Food: ₹6,000

- Travel: ₹3,000

- Other: ₹6,000

Savings left: ₹10,000

He takes a ₹3 lakh loan. EMI: ₹9,500

Now savings drop to ₹500.

One emergency, and he’s stuck.

This is how loans become traps.

Common Mistakes

- Looking only at EMI, not total cost

- Taking multiple loans at once

- Ignoring processing and late fees

- Borrowing without emergency planning

- Using loan for non-essential expenses

Pro Tips (Practical and Useful)

- Prepay whenever possible to reduce interest

- Choose shorter tenure if you can afford it

- Maintain a credit score above 750 for better rates

- Avoid loan apps with unclear charges

- Build an emergency fund to avoid future loans

Tools & Platforms

If you’re considering a loan, compare first.

Use platforms like:

- BankBazaar

- Paisabazaar

They help you check rates across banks and NBFCs.

For better planning, track expenses using:

- Walnut

Better tracking reduces your need for loans.

FAQs

1. Is taking a personal loan bad?

Not always. It’s bad if used for non-essential spending.

Good for emergencies or debt consolidation.

2. What is a safe EMI percentage?

Keep EMIs below 20–25% of your monthly income.

3. Can I close a personal loan early?

Yes. Most lenders allow prepayment.

But check for prepayment charges.

4. Which is better: credit card or personal loan?

Personal loan usually has lower interest than credit cards.

But both are risky if misused.

5. Do personal loans affect credit score?

Yes. Timely payment improves score.

Missed EMIs damage it badly.

Conclusion

Personal loans are not evil. But they are expensive.

Use them only when needed.

Not for lifestyle upgrades.

If you can’t repay comfortably, don’t take it.

Simple rule: borrow only when you have a clear exit plan.