You’re earning ₹40k–₹1L per month.

Rent feels like “wasted money.”

Family says, “Buy a house. It’s an asset.”

But EMIs look scary. And prices keep rising.

So what actually makes sense in 2026?

This guide breaks it down clearly. No emotional bias. Only numbers and real-life logic.

QUICK ANSWER

Rent vs Buy House in India — What should you do?

- Rent if you value flexibility and lower monthly pressure

- Buy if you have stable income and plan to stay 10+ years

- If EMI > 30–35% of income, buying is risky

- Renting + investing the difference often beats buying financially

- Buying is emotional security, not always financial smartness

In India, home buying is emotional.

But money doesn’t care about emotions.

You’re comparing two things:

- Renting = paying for flexibility

- Buying = locking money into one asset

The mistake? People compare rent vs EMI directly.

That’s wrong.

You must compare total cost + opportunity loss.

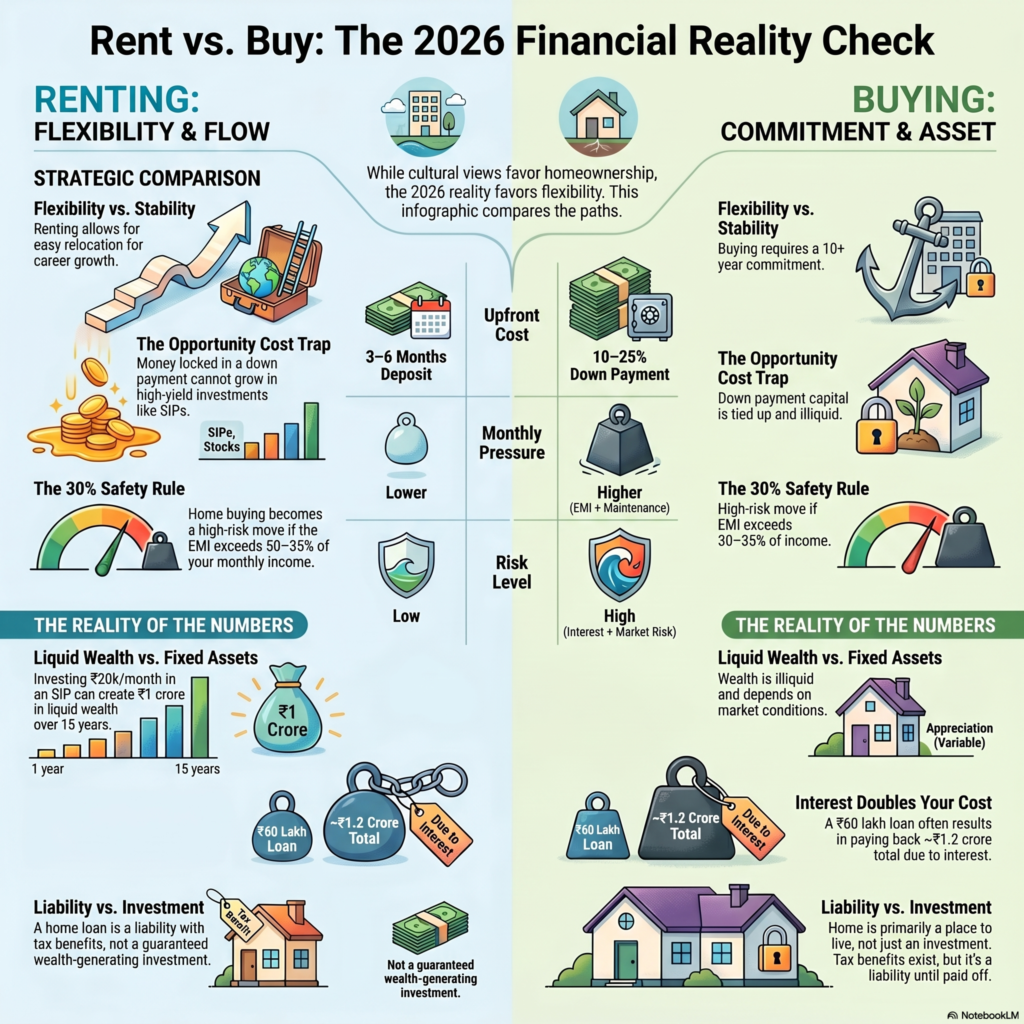

RENT VS BUY HOUSE IN INDIA (2026 COMPARISON)

| Factor | Renting | Buying |

| Monthly Cost | Lower | Higher (EMI + maintenance) |

| Flexibility | High | Zero |

| Upfront Cost | Deposit (3–6 months) | Down payment (10–25%) |

| Investment Growth | You can invest savings | Money locked in house |

| Risk | Low | High (loan + property risk) |

| Emotional Value | Low | High |

| Best For | Job switchers, early career | Stable income, long stay |

PROS & CONS

Renting

Pros

- Low commitment

- Easy relocation

- More money for SIPs

Cons

- No asset creation

- Rent increases

- No emotional ownership

Buying

Pros

- Long-term asset

- Stability

- Tax benefits (home loan)

Cons

- Huge EMI pressure

- Interest doubles cost

- No flexibility

REAL-LIFE EXAMPLE (INDIAN SCENARIO)

Let’s break this with real numbers.

Scenario:

- Salary: ₹80,000/month

- City: Chennai

Option 1: Renting

- Rent: ₹20,000

- Investment (SIP): ₹20,000

- Return (12% for 15 years): ~₹1 crore

Option 2: Buying

- House cost: ₹70 lakh

- Down payment: ₹10 lakh

- Loan: ₹60 lakh

- EMI: ~₹50,000 for 20 years

Total paid: ~₹1.2 crore

Reality Check

- Renting + investing = ₹1 crore liquid wealth

- Buying = house worth maybe ₹1–1.5 crore (not liquid)

Now ask yourself:

Would you rather have:

- A house you live in

- Or money that gives freedom?

COMMON MISTAKES PEOPLE MAKE

- Comparing rent with EMI only

Ignoring maintenance, taxes, interest. - Buying too early

No stable income, no savings. - Using 90% loan eligibility

Bank says yes. That doesn’t mean you should. - Ignoring job mobility

You may not stay in the same city. - Overestimating property appreciation

Real estate is slow, not magic.

PRO TIPS

- Keep EMI below 30% of income

- Always have 6 months emergency fund before buying

- Invest first, then think of buying

- Don’t buy just because “others are buying”

- Calculate total cost, not just EMI

TOOLS & PLATFORMS

Before deciding, run your numbers properly.

Use:

- SIP calculators on Groww or Zerodha

- Home loan EMI calculators from HDFC Bank or SBI

Track both scenarios side by side.

Don’t guess. Calculate.

FAQ

1. Is renting better than buying a house in India?

Depends on your situation.

If you move often or earn less, rent.

If stable for 10+ years, buying makes sense.

2. What salary is needed to buy a house in India?

Ideally ₹80k+ monthly.

EMI should not cross 30–35% of income.

3. Is home loan a good investment?

No. It’s a liability with tax benefits.

Not a pure investment.

4. Does property always increase in value?

No. Many areas stagnate for years.

Don’t assume guaranteed returns.

5. Should I buy a house or invest in SIP?

For most young Indians:

Invest first, buy later.

CONCLUSION

Here’s the blunt truth:

Buying a house is not always a smart financial decision.

It’s a lifestyle choice.

If your income is unstable, don’t buy.

If you want freedom, don’t rush.

Renting is not wasting money.

It’s buying flexibility.

But if you’re stable, disciplined, and staying long-term, buying works.

No shortcuts here.

Run the numbers. Then decide.