You want to grow your money safely.

But every time you ask, people say different things.

“FD is safe.”

“SIP gives higher returns.”

Now you’re stuck.

Here’s the truth: both work. But not for the same goal.

In this guide, you’ll see exactly which gives better returns in 10 years, with real numbers and clear logic.

Quick Answer

- SIP usually beats FD over 10 years due to higher market returns

- FD gives fixed, low-risk returns (around 6–7% yearly)

- SIP returns vary but average 10–14% over long term

- Choose FD for safety and short-term goals

- Choose SIP for wealth creation and beating inflation

What Are SIP and FD?

SIP (Systematic Investment Plan)

You invest a fixed amount monthly in mutual funds.

Returns depend on market performance.

FD (Fixed Deposit)

You deposit money in a bank for fixed interest.

Returns are guaranteed.

Simple difference:

FD = safety

SIP = growth

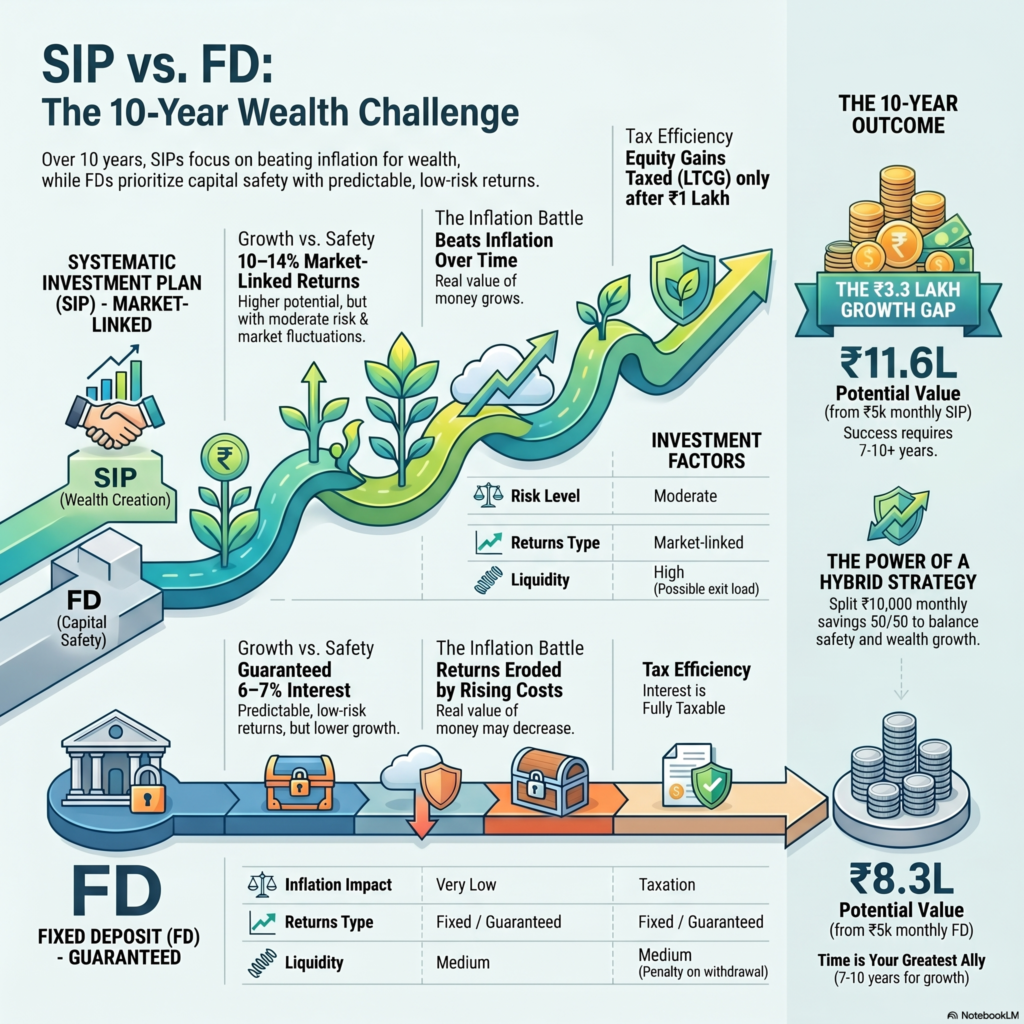

SIP vs FD in India: 10-Year Comparison

Returns Comparison (Realistic Scenario)

| Factor | SIP (Equity Mutual Fund) | FD (Bank Fixed Deposit) |

| Average Return | 10% – 14% | 6% – 7% |

| Risk | Moderate | Very Low |

| Returns Type | Market-linked | Fixed |

| Inflation Impact | Beats inflation | Often loses to inflation |

| Liquidity | High (with exit load) | Medium (penalty on withdrawal) |

| Tax | LTCG after ₹1L | Fully taxable |

Example: ₹5,000 Monthly Investment for 10 Years

Let’s remove theory and see actual numbers.

SIP Calculation (12% return):

- Monthly: ₹5,000

- Duration: 10 years

- Total Invested: ₹6,00,000

- Final Value: ~₹11,60,000

FD Calculation (7% return):

- Monthly equivalent investment

- Total Invested: ₹6,00,000

- Final Value: ~₹8,30,000

Difference: ~₹3,30,000 more with SIP

That’s not small. That’s the whole point.

Pros and Cons

SIP

Pros

- Higher long-term returns

- Beats inflation

- Builds wealth slowly

Cons

- Market fluctuations

- Requires patience

- Not ideal for short-term goals

FD

Pros

- Safe and predictable

- No market tension

- Good for emergency funds

Cons

- Low returns

- Tax reduces earnings

- Inflation eats value

Who Should Choose What?

Be honest with yourself.

Choose SIP if:

- You can stay invested for 7–10 years

- You want real wealth growth

- You can handle market ups and downs

Choose FD if:

- You need guaranteed returns

- You’re saving for short-term goals

- You can’t tolerate risk at all

If you pick FD for long-term wealth, you’re playing it too safe.

And that costs money.

Real-Life Example (Indian Scenario)

Karthick earns ₹35,000/month in Chennai.

Monthly expenses:

- Rent: ₹10,000

- Groceries: ₹6,000

- Bills + UPI spends: ₹5,000

- Misc: ₹4,000

Savings left: ₹10,000

What he does:

- ₹5,000 → SIP

- ₹5,000 → FD

After 10 years:

- SIP grows to ~₹11.6 lakh

- FD grows to ~₹8.3 lakh

Total: ~₹19.9 lakh

If Karthick had put everything in FD: ~₹16.6 lakh

He would lose ₹3+ lakh just by playing safe.

Common Mistakes

- Choosing FD for long-term wealth creation

- Stopping SIP during market dips

- Ignoring inflation impact

- Investing without clear goal

- Putting all money in one option

Pro Tips

- Start SIP early, even ₹1,000 is enough

- Increase SIP amount yearly

- Use FD only for emergency fund

- Stay invested at least 7–10 years

- Don’t check SIP returns daily

Tools & Platforms

If you’re starting SIP, use simple platforms like:

- Groww

- Zerodha Coin

For FD comparison and better rates, check:

- HDFC Bank

- ICICI Bank

Don’t overthink tools. Start first.

FAQs

1. Is SIP better than FD in India?

For long-term wealth, yes. SIP usually gives higher returns.

2. Is FD safer than SIP?

Yes. FD has almost zero risk. SIP depends on markets.

3. Can SIP give negative returns?

In short term, yes. Over 10 years, rarely.

4. Which is better for 5 years?

Mixed approach. SIP + FD works better.

5. Is SIP taxable?

Yes. Gains above ₹1 lakh taxed at 10%.

6. Can I do both SIP and FD?

That’s actually the smartest approach.

Conclusion

If your goal is safety, FD works.

If your goal is growth, SIP wins.

Over 10 years, the difference is not small.

It’s lakhs.

Stop trying to avoid risk completely.

Start managing it smartly.