Saving ₹5 lakhs is not a small achievement.

Most people either leave it in a savings account or put everything into one investment. Both are mistakes.

A good ₹5 lakh investment plan in India depends on three things:

- Your emergency needs

- Your risk tolerance

- Your financial goals

If used properly, ₹5 lakhs can create monthly income, long-term wealth, or financial security. This guide shows a practical investment plan for Indian beginners without confusing finance jargon.

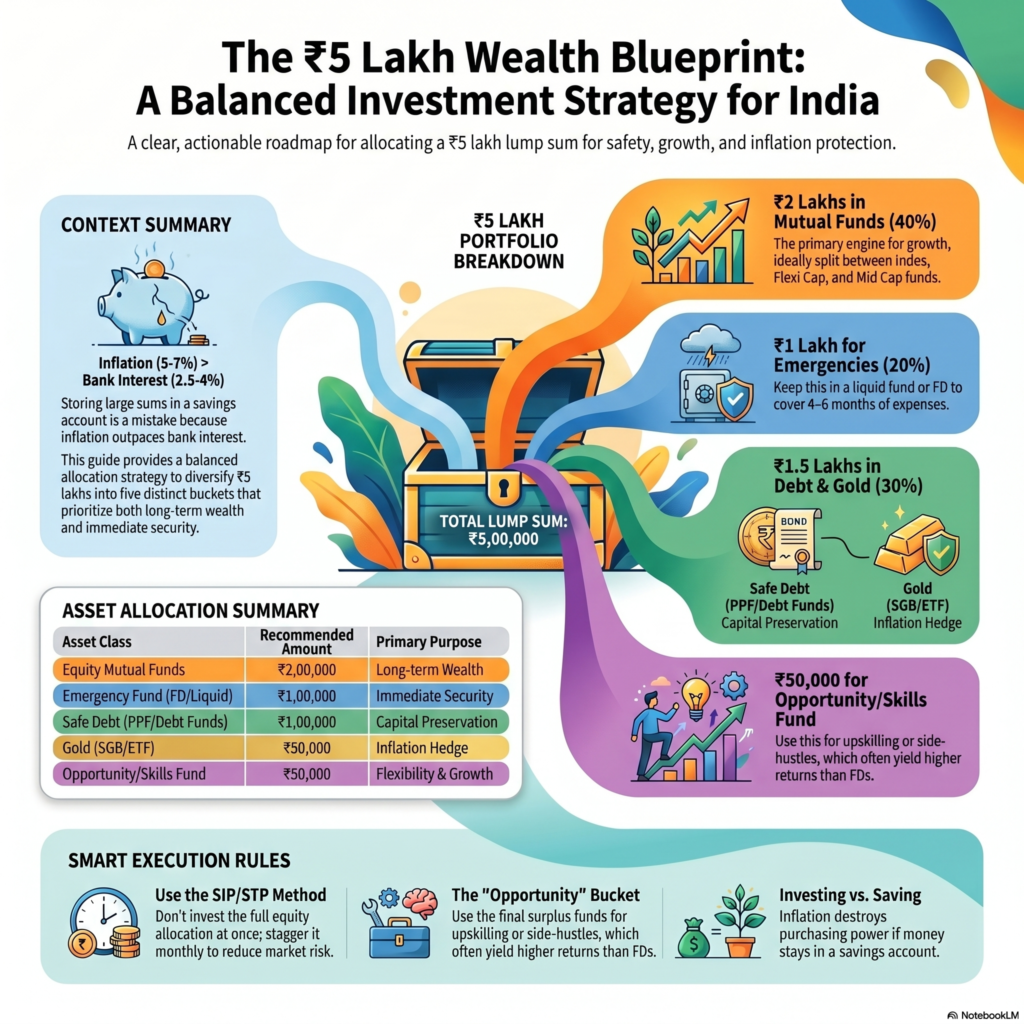

Quick Answer: Best Investment Plan for ₹5 Lakhs in India

Here’s a balanced investment allocation for most Indians:

- ₹1 lakh → Emergency fund in FD or liquid fund

- ₹2 lakhs → SIP + index mutual funds

- ₹1 lakh → Debt investments like PPF or short-term debt funds

- ₹50,000 → Gold ETF or Sovereign Gold Bonds

- ₹50,000 → High-growth or flexible investments

This plan balances:

- Safety

- Growth

- Liquidity

- Inflation protection

Best for:

- Salaried employees

- Beginners

- Middle-class families

- First-time investors

Why You Should Not Keep ₹5 Lakhs in Savings Account

Many Indians leave large savings in bank accounts.

That feels safe. But inflation quietly destroys the value.

Example:

- Savings account interest: 2.5%–4%

- Inflation in India: 5%–7%

Your money grows slower than expenses.

After 10 years, your purchasing power drops heavily.

That is why smart allocation matters more than simply saving money.

Best Investment Plan for ₹5 Lakhs in India

1. Keep ₹1 Lakh as Emergency Fund

What it is

Money for emergencies:

- Job loss

- Medical expenses

- Family emergencies

- Sudden repairs

Why it works

You avoid:

- Personal loans

- Credit card debt

- Breaking investments early

Where to keep it

Choose:

- High-interest savings account

- Liquid mutual fund

- Fixed deposit

Who should do this

Everyone.

No exceptions.

Action Step

Keep at least 4–6 months of expenses ready.

If your monthly expenses are ₹25,000:

- Emergency fund needed = ₹1–1.5 lakhs

2. Invest ₹2 Lakhs in Mutual Funds

This is where long-term wealth gets created.

Split Example

| Fund Type | Amount |

| Index Fund | ₹1,20,000 |

| Flexi Cap Fund | ₹50,000 |

| Mid Cap Fund | ₹30,000 |

Why Mutual Funds Work

- Professional management

- Better returns than FD

- Good for long-term investing

- Easy SIP options

Historically, quality equity mutual funds gave around 10%–14% annual returns over long periods.

Best Strategy

Do not invest entire ₹2 lakhs in one day.

Use STP or SIP method.

Example:

- Invest ₹25,000 monthly for 8 months

This reduces market timing risk.

Who Should Use Mutual Funds

Best for:

- Salaried employees

- Young investors

- People investing for 5+ years

Not ideal if:

- You panic during market falls

3. Put ₹1 Lakh in Safe Debt Investments

Not all money should chase high returns.

You need stability too.

Good Options

| Investment | Returns | Lock-in | Risk |

| PPF | 7%–8% | 15 years | Very low |

| FD | 6%–7% | Flexible | Low |

| Debt Mutual Funds | 6%–8% | Flexible | Moderate |

Best Choice for Beginners

- PPF for long-term safety

- FD for short-term goals

- Debt funds for tax efficiency

Action Step

If you already have EPF through salary:

- Use debt mutual funds or FD for diversification

4. Invest ₹50,000 in Gold

Gold is not for fast growth.

Gold is protection.

When markets crash or inflation rises, gold often performs well.

Best Gold Investments in India

Avoid heavy jewellery purchases.

Better options:

- Sovereign Gold Bonds (SGB)

- Gold ETF

- Digital gold only from trusted apps

Why Gold Helps

- Diversifies portfolio

- Reduces overall risk

- Useful during economic uncertainty

5. Keep ₹50,000 for Opportunities

This part gives flexibility.

Use it for:

- Business ideas

- Skill courses

- Stocks

- Side hustle setup

- REITs

- Travel or career upgrades

Most people ignore this.

But improving income potential often gives better returns than investments.

A ₹20,000 skill course can increase salary faster than an FD ever will.

Real-Life Example: ₹5 Lakh Investment Plan for an Indian Salaried Employee

Rahul is 29 years old.

Monthly salary: ₹55,000

Monthly expenses: ₹28,000

Existing savings: ₹5 lakhs

Here’s his allocation:

| Investment | Amount |

| Emergency FD | ₹1,20,000 |

| Index Mutual Funds | ₹1,50,000 |

| Flexi Cap Fund | ₹50,000 |

| PPF | ₹80,000 |

| Gold ETF | ₹50,000 |

| Skill Upgrade + Cash | ₹50,000 |

Expected outcome after 10 years:

- Potential portfolio value: ₹11–15 lakhs+

- Better financial security

- Lower debt risk

This assumes regular SIP continuation.

Common Mistakes People Make With ₹5 Lakhs Savings

Investing Everything in One Place

Many put all money into:

- FD

- Gold

- One stock

- One crypto coin

That is risky and inefficient.

Keeping Too Much Cash

Too much idle money loses value yearly because of inflation.

Chasing “Double Money” Schemes

If someone promises:

- Guaranteed high returns

- Fast profits

- No risk

Assume it is dangerous.

Buying Insurance as Investment

Traditional LIC-type plans often give poor returns.

Insurance and investing should usually stay separate.

Ignoring Taxes

Tax affects actual returns.

Always check:

- Capital gains tax

- FD taxation

- Debt fund taxation

Pro Tips for Investing ₹5 Lakhs Smartly

- Increase SIP yearly with salary hikes

- Use index funds if confused

- Avoid random stock tips from social media

- Review portfolio once every 6 months

- Keep investments simple

Complex portfolios usually perform worse for beginners.

Best Platforms and Apps for Investing in India

These platforms are beginner-friendly:

For fixed deposits:

Before investing:

- Compare charges

- Check lock-in periods

- Understand taxation

FAQ: ₹5 Lakhs Investment Plan India

Can I retire with ₹5 lakhs investment?

No.

₹5 lakhs alone is not enough for retirement in India.

But it is a strong starting point.

Is FD better than mutual funds?

FD is safer.

Mutual funds usually offer better long-term growth.

Both serve different purposes.

How much return can ₹5 lakhs generate?

Depends on allocation.

A balanced portfolio may generate:

- 8%–12% yearly average over long periods

Not guaranteed.

Should I invest lump sum or SIP?

For beginners:

- SIP or staggered investing is safer

Especially during volatile markets.

Is gold necessary in portfolio?

Not mandatory.

But 5%–10% gold allocation helps diversification.

Which mutual fund is best for beginners?

Index funds are usually easiest.

They are:

- Low-cost

- Simple

- Less dependent on fund managers

Conclusion

The best investment plan for ₹5 lakhs in India is not about finding one “perfect” investment.

It is about balance.

Keep some money safe.

Invest some for growth.

Protect against emergencies.

And improve your earning power.

A simple portfolio beats a complicated one for most people.

Do not chase fast returns.

Focus on:

- Consistency

- Diversification

- Long-term investing

That is what actually builds wealth in India.