You have some savings. Maybe ₹5,000 or ₹20,000 a month.

Now the confusion starts.

Should you go safe with FD?

Try SIP for higher returns?

Or buy gold like our parents suggest?

Pick wrong, and your money either grows too slow… or you panic and exit early.

In this guide, you’ll learn exactly where to invest between SIP vs FD vs Gold in India, based on your situation. No theory. Only practical decisions.

Quick Answer

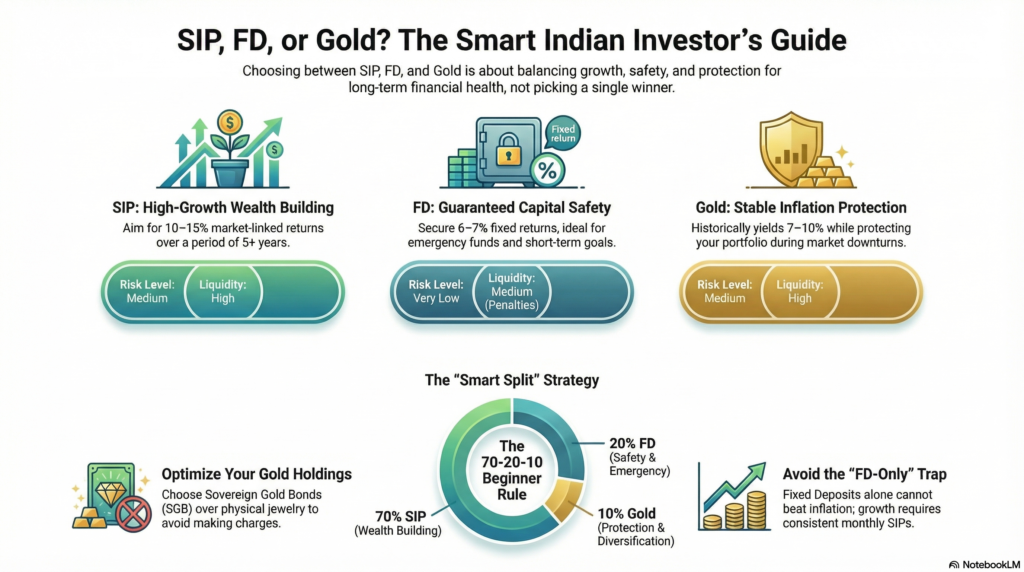

- Choose SIP if you want long-term wealth (5+ years)

- Choose FD if you want safety and fixed returns

- Choose Gold if you want protection against inflation

- Best strategy: Don’t pick one — combine all three

- Beginners should start with 70% SIP, 20% FD, 10% Gold

SIP vs FD vs Gold – Basic Understanding

Before comparing, understand this clearly:

- SIP (Systematic Investment Plan): Invest monthly in mutual funds

- FD (Fixed Deposit): Fixed return from bank for a fixed time

- Gold: Physical or digital asset that holds value over time

Simple truth:

- SIP = Growth

- FD = Safety

- Gold = Protection

SIP vs FD vs Gold – Detailed Comparison

| Factor | SIP (Mutual Funds) | FD (Fixed Deposit) | Gold |

| Returns | 10–15% (market-linked) | 6–7% (fixed) | 7–10% (average long-term) |

| Risk | Medium | Very low | Medium |

| Liquidity | High | Medium (penalty possible) | High |

| Inflation Protection | Yes | No | Yes |

| Best For | Wealth building | Capital safety | Diversification |

SIP vs FD vs Gold – Which Should You Choose?

1. SIP (Best for Wealth Creation)

What it is: Monthly investment into equity mutual funds

Why it works:

Markets grow over time. SIP averages your cost.

Who should use it:

- Salaried people

- Long-term investors

- Beginners willing to stay invested

Example:

₹5,000/month for 10 years at 12% = ~₹11.6 lakh

Action:

Start SIP in index or flexi-cap mutual funds.

2. FD (Best for Safety)

What it is: Bank deposit with fixed interest

Why it works:

Guaranteed returns. No market tension.

Who should use it:

- Emergency funds

- Risk-averse people

- Short-term goals (1–3 years)

Example:

₹1 lakh in FD at 7% for 3 years = ~₹1.23 lakh

Action:

Keep 6 months expenses in FD.

3. Gold (Best for Stability)

What it is: Physical gold, digital gold, or sovereign bonds

Why it works:

Gold rises when markets fall or inflation rises.

Who should use it:

- Conservative investors

- Portfolio balancing

- Cultural buying (weddings)

Example:

Gold often grows 7–9% annually long-term

Action:

Buy Sovereign Gold Bonds instead of jewellery.

Real-Life Example

Let’s say Ravi earns ₹35,000/month in Chennai.

Monthly Allocation:

- ₹10,000 savings

Here’s a smart split:

- ₹6,000 → SIP

- ₹3,000 → FD

- ₹1,000 → Gold

After 5 years:

- SIP grows aggressively

- FD gives stability

- Gold protects during market dips

Result: Balanced growth + low stress

Common Mistakes People Make

- Putting all money in FD

→ Safe, but loses against inflation - Investing in SIP, then stopping in market crash

→ Biggest wealth killer - Buying gold jewellery as investment

→ Making charges destroy returns - No diversification

→ Either too risky or too slow - Chasing returns blindly

→ Leads to panic decisions

Pro Tips

- Start SIP first, not FD

- Use FD only for emergency fund

- Prefer Sovereign Gold Bonds over physical gold

- Increase SIP amount every year

- Stay invested for at least 5 years

Where to Invest (Tools & Platforms)

You can start easily using:

- SIP: Groww, Zerodha Coin, ET Money

- FD: Any major bank or small finance banks

- Gold: RBI Sovereign Gold Bonds or trusted apps

Don’t overthink tools. Focus on consistency.

FAQ

1. Which is better: SIP vs FD vs Gold?

SIP is best for growth. FD for safety. Gold for stability. Combine all three.

2. Is SIP safer than FD?

No. SIP has market risk. But gives higher returns long-term.

3. How much should I invest in gold?

Keep gold at 5–10% of your portfolio. Not more.

4. Can I lose money in SIP?

Yes, short-term. But long-term (5+ years), risk reduces significantly.

5. Is FD enough for retirement?

No. FD alone cannot beat inflation. You need SIP.

6. What is the safest investment in India?

FD is safest. But it won’t grow your wealth.

Conclusion

Stop trying to choose just one.

That’s the mistake.

- SIP builds wealth

- FD protects you

- Gold balances your portfolio

If you want real results:

Start SIP today.

Keep FD for safety.

Add a little gold.

That’s how smart Indians invest.