Ever noticed your EMI suddenly going up… or your FD giving better returns?

That’s not random. It’s because the Reserve Bank of India changed interest rates.

Most people ignore this. Big mistake.

In this guide, you’ll learn exactly how RBI interest rates affect your loans and savings in India — and what to do about it.

QUICK ANSWER

- When RBI increases repo rate → loan EMIs increase

- When RBI cuts repo rate → EMIs reduce (slowly, not instantly)

- Savings account and FD interest rates rise when rates go up

- Loans become expensive, saving becomes more rewarding

- You should adjust loans, SIPs, and FDs based on rate cycle

RBI controls money flow using something called the repo rate.

This is the rate at which banks borrow money from RBI.

Simple logic:

- Higher repo rate → banks borrow costly → you pay more interest

- Lower repo rate → banks borrow cheap → you pay less interest

That’s the chain reaction.

HOW RBI INTEREST RATES AFFECT YOUR LOANS AND SAVINGS

1. Impact on Home Loans

What happens:

When RBI increases rates, home loan interest increases.

Example:

You have a ₹30 lakh home loan at 8%.

If rate becomes 9%, your EMI jumps or tenure increases.

Action:

- Choose floating rate loans only if you can handle fluctuations

- Refinance when rates drop

2. Impact on Personal Loans

What happens:

Personal loans become expensive very fast.

These loans already have high interest (10%–18%).

Example:

₹5 lakh personal loan at 13% → becomes 15%

Your EMI shoots up noticeably.

Action:

- Avoid taking new loans during high rate periods

- Prepay existing loans if possible

3. Impact on Credit Cards

What happens:

Indirect effect. Banks tighten lending.

Interest rates stay high (30%+ yearly), but approvals get stricter.

Action:

- Don’t carry balances

- Pay full bill every month

4. Impact on Fixed Deposits (FDs)

What happens:

FD interest rates increase when RBI raises rates.

Example:

FD rates move from 6% → 7.5%

Now your savings earn more.

Action:

- Lock FDs when rates peak

- Avoid long-term FD during low rate cycle

5. Impact on Savings Accounts

What happens:

Savings account interest increases slightly.

But not as much as loans increase.

Banks protect their profit.

Action:

- Don’t rely on savings account for growth

- Move idle money to FD or liquid funds

6. Impact on Investments (SIP, Stocks, Mutual Funds)

What happens:

- High interest rates → stock market may slow down

- Low interest rates → markets usually rise

Why:

Cheap money boosts business growth.

Action:

- Continue SIPs regardless of rate changes

- Don’t stop investing due to short-term rate hikes

REAL-LIFE EXAMPLE

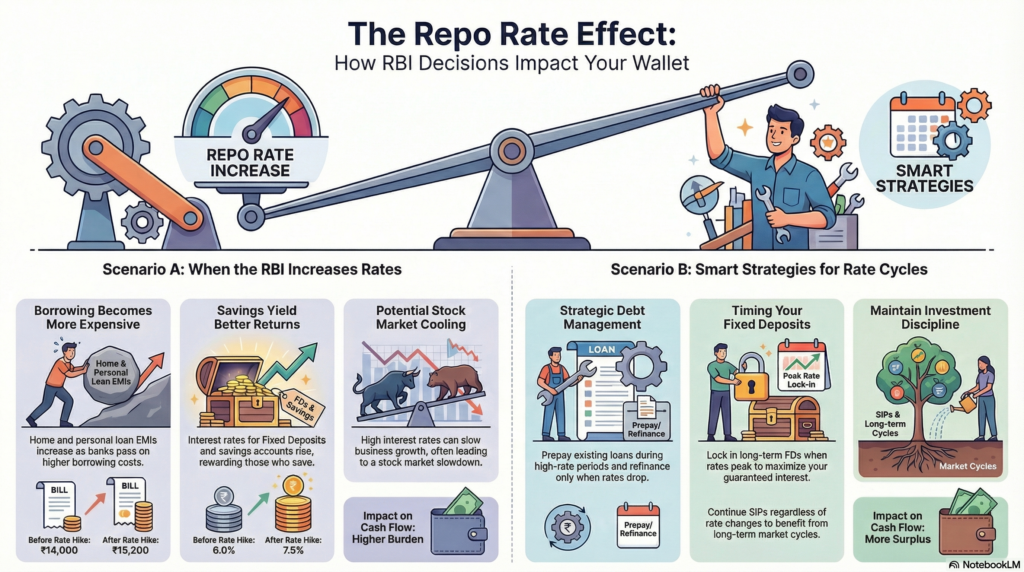

Let’s take Ravi, earning ₹35,000/month.

Before RBI Rate Hike:

- Home loan EMI: ₹14,000

- FD return: 6%

- Savings: ₹5,000/month

After RBI Rate Hike:

- EMI increases to ₹15,200

- FD return rises to 7.5%

Result:

- Extra EMI burden: ₹1,200

- Better savings return

Smart move:

- Ravi shifts ₹1 lakh into FD at higher rate

- Cuts unnecessary expenses

- Avoids taking new loans

COMMON MISTAKES

- Ignoring EMI changes until it’s too late

- Taking loans during high interest cycle

- Locking FDs when rates are low

- Stopping SIPs during rate hikes

- Not comparing loan refinancing options

PRO TIPS

- Track RBI policy meetings (every 2 months)

- Prepay loans when rates are rising

- Lock FDs only when rates peak

- Keep emergency fund in liquid funds

- Use EMI calculators before taking loans

If you want to act on this:

- Use apps like Groww or Zerodha Coin for SIPs

- Compare loans on platforms like BankBazaar

- Check FD rates across banks before investing

Small decisions here can save lakhs over time.

FAQ SECTION

1. What is RBI repo rate?

It is the interest rate at which RBI lends money to banks.

2. How often does RBI change interest rates?

Usually every 2 months in monetary policy meetings.

3. Do all loans get affected immediately?

No. Floating rate loans change faster than fixed loans.

4. Is it good when RBI increases interest rates?

Good for savers, bad for borrowers.

5. Should I close my loan when rates increase?

Not always. But consider prepayment or refinancing.

6. Do FD rates increase instantly after RBI hike?

Not instantly. Banks take time to adjust.

CONCLUSION

RBI interest rates directly control your money flow.

- Loans become costly when rates rise

- Savings give better returns

- Timing matters more than you think

If you ignore this, you lose money silently.

If you use it smartly, you stay ahead.

Track rates. Adjust your strategy. That’s how you win.