A low CIBIL score can quietly destroy your financial life.

Banks reject your loan. Credit cards get denied. Even if approved, interest rates become painful.

Most people in India only check their CIBIL score after rejection. That’s backward.

The good news? You can improve your CIBIL score faster than most people think. But you need to fix the right things first.

This guide explains what actually works in India in 2026.

Quick Answer: How to Improve Your CIBIL Score Fast

If you want to improve your CIBIL score quickly in India:

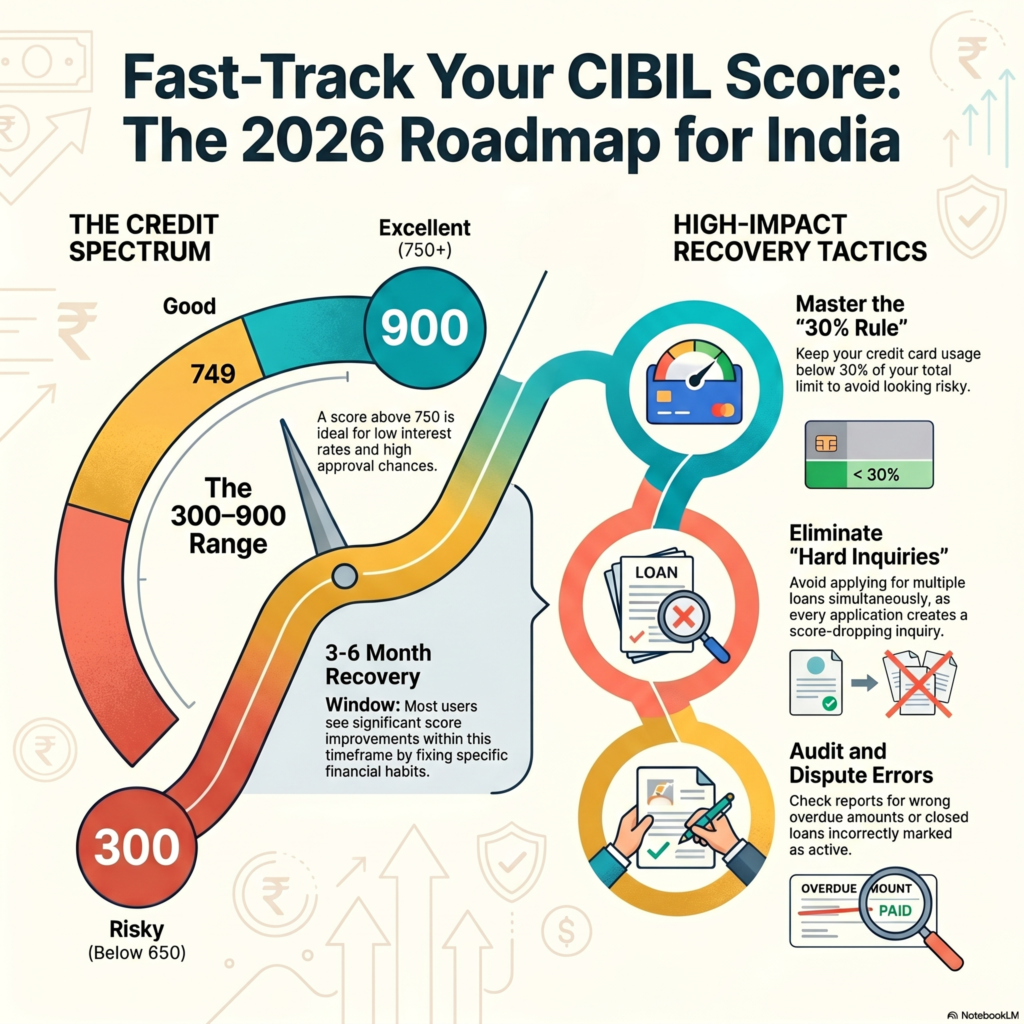

- Pay all EMIs and credit card bills on time

- Keep credit card usage below 30%

- Clear overdue payments immediately

- Avoid applying for multiple loans together

- Keep old credit cards active

Most people see noticeable improvement within 3–6 months.

What Is a CIBIL Score?

A CIBIL score is a 3-digit number between 300 and 900.

It shows how responsibly you handle credit.

Banks use it before approving:

- Personal loans

- Home loans

- Car loans

- Credit cards

- Buy Now Pay Later apps

Ideal CIBIL Score Range in India

| Score | Meaning |

| 750+ | Excellent |

| 700–749 | Good |

| 650–699 | Average |

| Below 650 | Risky |

A score above 750 gives better approval chances and lower interest rates.

How to Improve Your CIBIL Score Fast in India

1. Pay Every EMI and Credit Card Bill on Time

This matters the most.

Payment history contributes heavily to your CIBIL score.

Even one missed EMI can hurt badly.

Example

Rahul misses a ₹2,500 credit card payment for 45 days.

His score drops from 760 to 705.

That single mistake affects future loan approvals.

Action Step

- Enable auto-pay for EMIs

- Set UPI reminders

- Pay at least 2 days before due date

Do not rely on memory.

2. Reduce Your Credit Card Usage

High credit usage signals financial stress.

This is called Credit Utilization Ratio.

If your card limit is ₹1 lakh, try using less than ₹30,000.

Credit Utilization Ratio=Credit UsedTotal Credit Limit×100\text{Credit Utilization Ratio} = \frac{\text{Credit Used}}{\text{Total Credit Limit}} \times 100Credit Utilization Ratio=Total Credit LimitCredit Used×100

Why It Works

Banks prefer people who use credit carefully.

Maxing out cards every month looks risky.

Example

- Card limit: ₹50,000

- Monthly spending: ₹48,000

That is dangerous for your score.

Instead:

- Split expenses across cards

- Increase card limit if income improved

- Pay card bills before statement generation date

3. Clear Outstanding Dues Immediately

Old unpaid loans destroy your score.

Especially:

- Personal loans

- Credit card settlements

- BNPL dues

- App-based instant loans

Many people ignore small overdue amounts. That’s a mistake.

Even a ₹1,000 unpaid balance can stay in your report for years.

Action Step

- Download your CIBIL report

- Identify overdue accounts

- Negotiate and close dues properly

- Ask for “No Dues Certificate”

Never leave accounts half-settled without documentation.

4. Stop Applying for Multiple Loans

Every loan application creates a “hard inquiry”.

Too many inquiries reduce your score.

Common Mistake

People apply everywhere after one rejection:

- HDFC Bank

- ICICI Bank

- SBI

- Loan apps

- NBFCs

That makes the situation worse.

Better Approach

- Check eligibility first

- Apply selectively

- Wait before reapplying

One or two inquiries are fine.

Ten inquiries in one month looks desperate.

5. Keep Old Credit Cards Active

Old accounts help your score.

They increase your credit history length.

Many people close their first credit card after getting a premium one.

Bad move.

Why It Helps

Banks trust borrowers with long credit history.

A 7-year-old card improves credibility.

Action Step

Use old cards occasionally for:

- Netflix

- Electricity bill

- Mobile recharge

Then pay full bill immediately.

6. Check Your CIBIL Report for Errors

Credit reports in India often contain mistakes.

Yes, seriously.

You may find:

- Wrong overdue amount

- Closed loan marked active

- Someone else’s loan

- Duplicate entries

Action Step

Check your report from:

- TransUnion CIBIL

- Experian

- CRIF High Mark

Dispute incorrect entries immediately.

This alone can improve scores fast.

7. Avoid Loan Settlement If Possible

Settlement is different from closure.

Banks may mark your account as “Settled”.

That damages your profile badly.

Example

Suppose you owe ₹80,000.

Bank accepts ₹45,000 settlement.

Sounds good temporarily.

But future lenders now see you as someone who did not repay fully.

Better Option

Try restructuring or full closure.

Settlement should be the last option.

8. Use a Secured Credit Card If Your Score Is Very Low

If banks reject you everywhere, start small.

Use FD-backed secured cards.

Banks like:

- ICICI Bank

- IDFC FIRST Bank

- Axis Bank

offer secured cards against fixed deposits.

How It Helps

You rebuild payment history safely.

Use small amounts monthly.

Pay full dues on time.

Many people recover from 550 to 700+ this way.

Real-Life Example: Improving CIBIL Score in India

Situation

Amit earns ₹38,000 monthly in Chennai.

Monthly expenses:

| Expense | Amount |

| Rent | ₹10,000 |

| Groceries | ₹6,000 |

| Bike EMI | ₹3,500 |

| UPI & fuel | ₹5,000 |

| Credit card dues | ₹18,000 |

Problems:

- Missed 2 EMIs

- Used 90% card limit

- Applied for 5 loan apps

His score dropped to 642.

What He Did

- Cleared overdue EMI

- Reduced card usage to 25%

- Stopped loan applications

- Used salary account for auto-pay

- Checked and fixed report errors

Result

After 5 months:

- Score improved to 741

- Got approved for a lower-interest personal loan

Not magic. Just disciplined fixes.

Common Mistakes That Destroy CIBIL Scores

Paying Only Minimum Due

Banks love this.

Your score won’t.

Interest keeps growing.

Taking Too Many BNPL Loans

Apps make borrowing look harmless.

But multiple small loans damage credit behavior.

Ignoring Small Dues

That forgotten ₹700 telecom bill can appear later.

And hurt your report.

Closing All Credit Cards

No active credit history can reduce scores over time.

Co-Signing Someone Else’s Loan

If they miss payments, your score suffers too.

Pro Tips to Improve Your CIBIL Score Faster

- Pay credit card bills twice monthly

- Keep utilization below 30%

- Avoid withdrawing cash using credit cards

- Maintain a mix of loan types

- Check score every 2–3 months

Consistency matters more than hacks.

Best Apps and Platforms to Track Credit Score

You can monitor your score using:

- OneScore

- CRED

- Paytm

- BankBazaar

These platforms also show:

- Credit report changes

- Loan eligibility

- Credit card offers

- EMI tracking

Useful if you struggle with tracking payments manually.

FAQ: How to Improve Your CIBIL Score Fast in India

How fast can I improve my CIBIL score?

Usually within 3–6 months if you fix payment issues and reduce utilization.

Does checking my own CIBIL score reduce it?

No.

Self-checking is called a soft inquiry.

It does not affect your score.

Can salary increase improve CIBIL score?

Not directly.

But higher income helps manage loans better.

Is 650 a bad CIBIL score?

It is below ideal.

Loan approvals become harder below 700.

Can I get a personal loan with low CIBIL score?

Yes, but interest rates become higher.

NBFCs may approve risky borrowers.

Should I close unused credit cards?

Not always.

Older cards help credit history length.

Close only if annual fees are high.

Conclusion

Improving your CIBIL score is not complicated.

But most people delay fixing obvious problems.

Late payments, high card usage, and random loan applications quietly destroy scores.

Focus on basics:

- Pay on time

- Use less credit

- Avoid unnecessary loans

- Monitor your report regularly

Do that consistently for a few months.

Your score will improve. And borrowing becomes cheaper.