Milk price went up. Rent increased. Petrol is unpredictable.

But your salary? Almost the same.

This is not bad luck. This is inflation in India.

If you feel your money is losing value every year, you’re right.

In this guide, you’ll understand why prices keep rising and what you can actually do about it.

QUICK ANSWER

Inflation in India means rising prices and decreasing purchasing power.

Here’s why everything is getting expensive:

- Demand is increasing faster than supply

- Fuel prices impact almost every product

- Government policies and taxes affect pricing

- Currency value changes increase import costs

- Global events (wars, supply chains) push prices up

Action: If your income doesn’t grow faster than inflation, you’re losing money.

WHAT IS INFLATION IN INDIA? (SIMPLE EXPLANATION)

Inflation means the same ₹100 buys less over time.

Example:

- 2015: ₹100 → full grocery bag

- 2026: ₹100 → maybe 3–4 items

That difference is inflation.

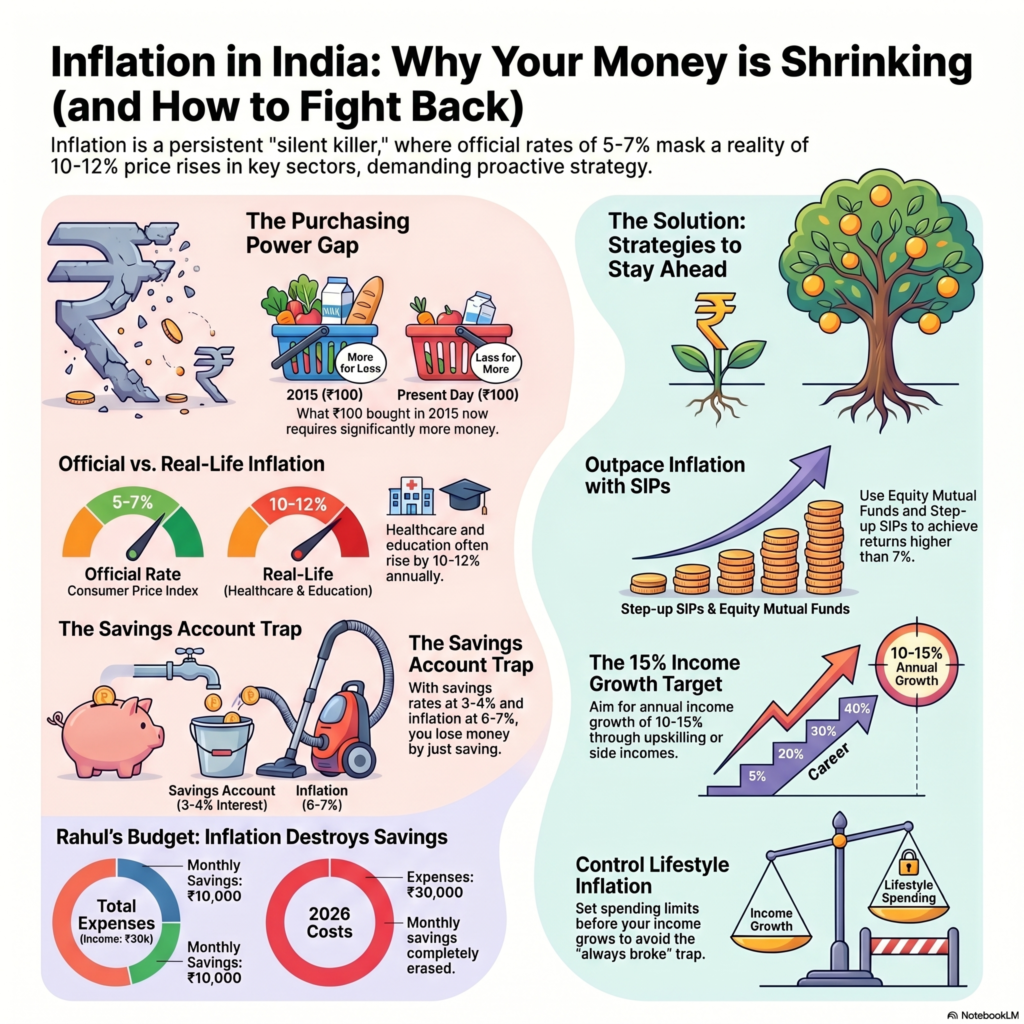

In India, average inflation stays around 5–7% yearly.

But real-life inflation (rent, school fees, healthcare) feels like 10–12%.

That gap is what hurts you.

WHY INFLATION IN INDIA IS RISING (REAL REASONS)

1. Fuel Prices Control Everything

Transport cost increases → everything becomes expensive.

Example:

- Diesel price ↑ → vegetables cost ↑ → delivery charges ↑

Action: Track fuel trends. Expect price hikes during global tensions.

2. High Demand, Limited Supply

India’s population is growing.

Demand for houses, food, jobs is rising.

Supply can’t keep up.

Result? Prices shoot up.

Action: Lock long-term costs early (rent agreements, school fees planning).

3. Government Taxes & Policies

GST, import duties, and subsidies directly affect prices.

Example:

- Higher tax on electronics → mobiles cost more

Action: Buy big items during policy-friendly periods (sales, tax cuts).

4. Rupee Value vs Dollar

India imports oil, electronics, gold.

If ₹ weakens:

- Imports become expensive

- Prices increase locally

Action: Avoid unnecessary imported luxury spending.

5. Global Factors (You Can’t Ignore This)

War, pandemics, supply chain issues.

These affect:

- Oil

- Food

- Raw materials

India doesn’t operate in isolation.

Action: Build buffer savings. Don’t assume stability.

HOW INFLATION AFFECTS YOU DIRECTLY

- Your savings lose value

- Fixed salary becomes weaker

- EMIs feel heavier

- Future goals become expensive

If your money grows slower than inflation, you’re falling behind.

REAL-LIFE INDIAN EXAMPLE (₹ BREAKDOWN)

Rahul earns ₹30,000/month

2020 Expenses:

- Rent: ₹8,000

- Groceries: ₹5,000

- Transport: ₹2,000

- Misc: ₹5,000

- Savings: ₹10,000

2026 Expenses:

- Rent: ₹12,000

- Groceries: ₹8,000

- Transport: ₹4,000

- Misc: ₹6,000

- Savings: ₹0

Income same. Expenses doubled.

This is inflation killing savings silently.

WHAT YOU SHOULD DO (PRACTICAL STRATEGY)

Step 1: Increase Income (Non-Negotiable)

Inflation won’t slow down for you.

Options:

- Job switch

- Freelancing

- Side income

Action: Aim minimum 10–15% income growth yearly.

Step 2: Don’t Rely on Savings Alone

Savings account gives ~3–4%.

Inflation = 6–7%.

You are losing money.

Action: Start SIP in mutual funds (long-term).

Step 3: Invest to Beat Inflation

Options:

- Equity Mutual Funds (SIP)

- Index Funds

- PPF (safe but slower)

Action: Combine safety + growth.

Step 4: Control Lifestyle Inflation

Income increased → expenses increased → still broke.

That’s the trap.

Action: Fix spending limits before income grows.

Step 5: Track Expenses Monthly

If you don’t track, you lose control.

Use:

- UPI apps insights

- Expense tracking apps

Action: Review spending weekly.

COMMON MISTAKES PEOPLE MAKE

- Keeping all money in savings account

- Ignoring small price increases

- Delaying investments

- Depending only on salary

- Upgrading lifestyle too fast

These are not small mistakes.

They destroy financial stability.

PRO TIPS

- Increase SIP amount yearly (step-up SIP)

- Avoid long-term fixed deposits only

- Buy insurance early (cost rises with inflation)

- Lock interest rates when low (home loan)

- Keep 6-month emergency fund

If you’re serious about beating inflation:

- Start SIP using platforms like Groww or Zerodha

- Use budgeting apps like Walnut or Money Manager

- Compare high-interest savings or sweep FD accounts

Don’t overthink. Start small. Increase later.

FAQ SECTION

1. What is the current inflation rate in India?

Usually around 5–7%, but real expenses feel higher.

2. Is inflation always bad?

Not always. Moderate inflation means economic growth.

High inflation destroys purchasing power.

3. How to protect money from inflation in India?

Invest in equity, mutual funds, and assets that grow faster than inflation.

4. Is FD good during inflation?

No. FD returns are often lower than inflation.

5. Why does salary not increase like inflation?

Because companies control costs. Market decides salary growth.

6. Does gold beat inflation?

Sometimes. But not consistently. Use it as a hedge, not main investment.

CONCLUSION

Inflation in India is not temporary.

It’s constant and unavoidable.

You have two choices:

- Ignore it and lose money silently

- Or act early and stay ahead

Increase income. Invest smart. Control spending.

If your money is not growing faster than inflation,

you are going backwards.