Money stress is not about low income.

It’s about lack of clarity.

You earn, you spend, and suddenly your account is empty.

Then guilt, tension, and overthinking start.

This guide will fix that.

You’ll learn how to manage money without stress using a simple Indian mindset. No complicated rules. Just practical systems that work on ₹20,000 or ₹1 lakh salary.

Quick Answer

How to manage money without stress in India:

- Spend after saving, not before

- Use a simple 3-bucket system (needs, wants, future)

- Automate savings using SIPs or recurring deposits

- Track only 3–4 major expenses, not everything

- Avoid lifestyle upgrades after salary hikes

Why Most Indians Feel Stressed About Money (And How to Fix It)

Most Indians manage money emotionally, not logically.

We save randomly. Spend impulsively. Invest late.

Stress comes from uncertainty, not money itself.

Once you create a simple system, money becomes predictable.

Predictability = less stress.

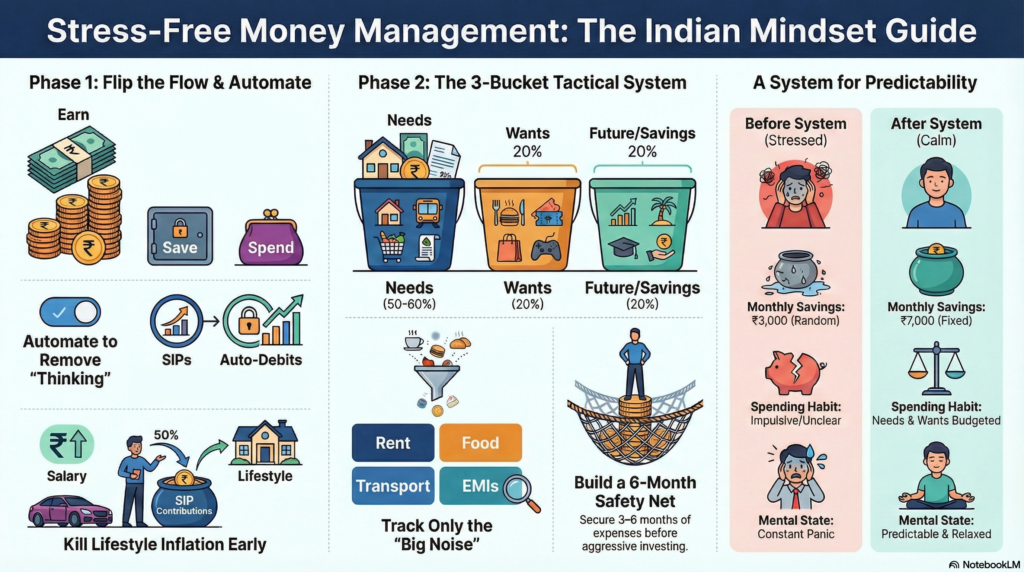

How to Manage Money Without Stress (Step-by-Step)

Step 1: Flip Your Money Flow

Explanation

Most people do this: Earn → Spend → Save leftover

This is wrong.

Correct flow: Earn → Save → Spend

Example

Salary ₹30,000

Save ₹6,000 first

Spend remaining ₹24,000

Action

Set auto-debit for savings on salary day.

Use apps like Groww or ET Money.

Step 2: Use the 3-Bucket System

Explanation

Don’t overcomplicate budgets.

Just split money into 3 parts:

- Needs (rent, food, bills)

- Wants (movies, eating out)

- Future (savings, investments)

Example

₹30,000 salary:

- Needs → ₹18,000

- Wants → ₹6,000

- Future → ₹6,000

Action

Open separate bank accounts or use app categories.

Step 3: Automate Investments (Remove Thinking)

Explanation

Thinking causes stress. Automation removes it.

Example

Set SIP of ₹3,000 in index fund monthly.

No decision needed every month.

Action

Start SIP via Zerodha Coin or Paytm Money.

Step 4: Track Only What Matters

Explanation

Tracking every chai is useless.

Track big categories only:

- Rent

- Food

- Transport

- EMIs

Example

If food expense jumps from ₹4,000 to ₹7,000, fix it.

Ignore small noise.

Action

Use simple notes or apps like Walnut.

Step 5: Kill Lifestyle Inflation Early

Explanation

Salary increases → expenses increase → stress stays.

This is the trap.

Example

Salary goes from ₹30K to ₹40K

Don’t upgrade everything immediately.

Save the extra ₹10K first.

Action

Increase SIP, not spending.

Real-Life Example (₹ Based)

Rahul, age 26, earns ₹35,000 in Chennai.

Before:

- Rent: ₹10,000

- Food + Swiggy: ₹8,000

- Bike EMI: ₹4,000

- Random spends: ₹10,000

- Savings: ₹3,000

Always stressed.

After system:

- Savings first: ₹7,000

- Needs: ₹18,000

- Wants: ₹10,000

He reduced Swiggy, controlled random spends.

Result: ₹7K consistent savings, no panic at month end.

Common Mistakes

- Saving whatever is left

- Tracking too many small expenses

- Investing without emergency fund

- Copying others’ lifestyle

- Ignoring insurance (health/term)

Pro Tips

- Keep 3–6 months expenses as emergency fund

- Use UPI but check weekly totals

- Avoid too many subscriptions

- Take health insurance early (cheap now, expensive later)

- Review money once a week, not daily

Tools & Platforms

If you want a stress-free system:

- Start SIP using Groww

- Track spending using Walnut

- Compare insurance on Policybazaar

Don’t overthink tools. Pick one and stick to it.

FAQ Section

1. How much should I save monthly in India?

At least 20% of income. Start with 10% if income is low.

2. Can I manage money without budgeting apps?

Yes. A simple 3-bucket system works fine.

3. What is the biggest reason for money stress?

Unclear spending and no fixed system.

4. Should I invest or save first?

Save emergency fund first. Then invest.

5. Is ₹30,000 salary enough to save?

Yes. Even ₹3,000–₹6,000 monthly is possible with control.

Conclusion

Money stress is not about how much you earn.

It’s about how predictable your system is.

- Save first

- Keep it simple

- Automate everything

Do this, and your money stops controlling you.