You finally have some savings.

But now comes the real problem — where to invest?

Everyone says “mutual funds”, “stocks”, “FD”, “crypto”… and you end up confused.

If you pick wrong, you lose money or waste years.

This guide cuts the noise.

You’ll learn the best investment options for beginners in India (2026) — simple, practical, and actually usable with ₹5,000–₹30,000 income.

Quick Answer

Best investment options for beginners in India:

- Mutual Funds (SIP) – best for long-term wealth

- Fixed Deposits (FD) – safe but low returns

- Public Provident Fund (PPF) – tax-free long-term savings

- Recurring Deposits (RD) – disciplined saving habit

- Direct Stocks – only after basic learning

- Gold (Digital/ETF) – for stability, not growth

Start with SIP + PPF combination. Avoid jumping into stocks blindly.

Investing is not about getting rich fast.

It’s about:

- Protecting money from inflation

- Growing wealth slowly

- Avoiding big mistakes

If you earn ₹20k–₹40k/month, your first goal is:

Consistency > High returns

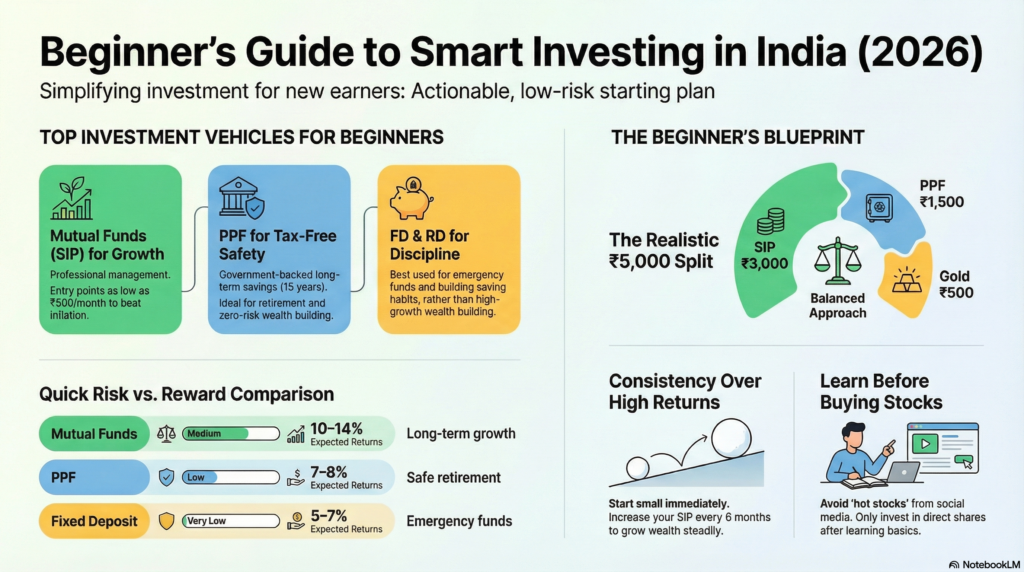

Best Investment Options for Beginners in India

1. Mutual Funds (SIP) – Best Starting Point

What it is:

You invest a fixed amount monthly in a fund.

Why it works:

- Managed by professionals

- Low entry (₹500/month)

- Beats inflation over time

Who should use it:

Anyone starting with ₹1,000–₹10,000/month.

Example:

₹2,000/month SIP for 10 years → ~₹4–5 lakh (approx)

Action:

Start SIP using apps like Groww or Zerodha Coin

2. Public Provident Fund (PPF) – Safe + Tax-Free

What it is:

Government-backed long-term investment (15 years).

Why it works:

- Tax-free returns

- No risk

- Good for retirement

Who should use it:

People who want safe, long-term savings.

Example:

₹5,000/month → ~₹16–18 lakh after 15 years

Action:

Open PPF in SBI, Post Office, or online banking.

3. Fixed Deposits (FD) – Safe but Limited

What it is:

Bank investment with fixed interest.

Why it works:

- Zero risk

- Guaranteed returns

Reality check:

Returns barely beat inflation.

Who should use it:

Emergency fund, not wealth building.

Example:

₹1 lakh FD → ~₹1.4 lakh in 5 years

Action:

Use FD only for stability, not growth.

4. Recurring Deposit (RD) – Discipline Tool

What it is:

Monthly fixed saving in bank.

Why it works:

- Builds saving habit

- No market risk

Who should use it:

Beginners who struggle to save.

Example:

₹3,000/month RD → ~₹2 lakh in 5 years

Action:

Set auto-debit RD in your bank.

5. Direct Stocks – High Risk, High Learning

What it is:

Buying shares of companies.

Why it works:

- High return potential

Reality check:

Most beginners lose money.

Who should use it:

Only after learning basics.

Example mistake:

Buying random “hot stocks” from YouTube.

Action:

Start with ₹1,000–₹2,000 only. Learn first.

6. Gold (Digital or ETF) – Stability Option

What it is:

Investing in gold without physical buying.

Why it works:

- Protects during crisis

- Hedge against inflation

Who should use it:

Diversification, not main investment.

Action:

Allocate max 10–15% of portfolio.

Comparison Table (Quick Clarity)

| Investment | Risk | Returns | Best For |

| Mutual Funds | Medium | 10–14% | Long-term growth |

| PPF | Low | 7–8% | Safe retirement |

| FD | Very Low | 5–7% | Emergency funds |

| RD | Very Low | 5–7% | Saving habit |

| Stocks | High | 0–20%+ | Experienced users |

| Gold | Low-Medium | 6–8% | Stability |

Real-Life Example (Indian Scenario)

Let’s say you earn ₹30,000/month.

Monthly plan:

- Rent + food: ₹18,000

- Expenses: ₹7,000

- Savings: ₹5,000

Smart investment split:

- ₹3,000 → SIP (Mutual Fund)

- ₹1,500 → PPF

- ₹500 → Gold

This is realistic. No fantasy.

Common Mistakes Beginners Make

- Investing in stocks without knowledge

- Expecting fast returns

- Putting all money in FD

- Ignoring inflation

- Stopping SIP during market fall

Pro Tips

- Start small, but start now

- Increase SIP every 6 months

- Don’t check returns daily

- Avoid “get rich quick” schemes

- Focus on 5+ year horizon

If you haven’t started yet:

- Open a free account on Groww for beginner-friendly investing

- Use Zerodha if you want to learn stocks later

Both are simple and widely used in India.

Start with SIP. Don’t overthink.

FAQ Section

1. What is the safest investment in India?

PPF and FD are safest. Government-backed or bank-secured.

2. Can I start investing with ₹500?

Yes. SIPs allow starting from ₹500/month.

3. Is mutual fund safe for beginners?

Yes, if you choose index or large-cap funds.

4. How much should I invest monthly?

Start with 10–20% of your income.

5. Should I invest in stocks as a beginner?

No. Learn first. Start small.

6. Which is better: FD or mutual fund?

FD is safer. Mutual funds give higher returns.

Conclusion

The best investment option for beginners in India is not complicated.

Start with:

- SIP for growth

- PPF for safety

Ignore noise. Avoid shortcuts.

Consistency will beat everything else.

Start this month. Not next year.