Earning ₹30,000 feels tight. Rent, food, travel… money disappears fast.

End of the month? Zero balance again.

This isn’t because you earn less. It’s because there’s no system.

In this guide, you’ll learn exactly how to save money on ₹30,000 salary in India—step by step, using real numbers and practical actions.

Quick Answer

To save money on a ₹30,000 salary in India:

- Follow a 50-30-20 rule (modified) based on reality

- Fix your rent and food costs first

- Automate saving ₹3,000–₹6,000 monthly

- Cut 3 silent expenses (subscriptions, eating out, impulse buys)

- Increase income with one side skill or freelance work

Saving is not about “cutting everything.”

It’s about controlling the big expenses first.

Most people fail because:

- They track small expenses

- Ignore rent, lifestyle, and habits

Your focus should be:

Fixed costs → habits → automation

Step-by-Step Plan to Save Money on ₹30,000 Salary

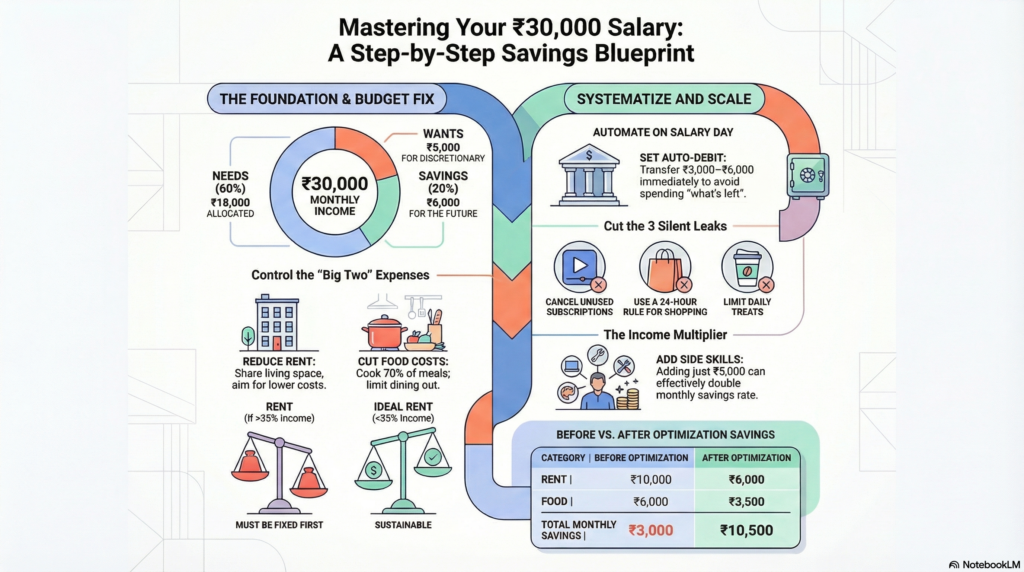

Step 1: Fix Your Budget (Realistic Version)

Forget textbook budgets.

Use this instead:

- Needs (60%) → ₹18,000

- Wants (20%) → ₹6,000

- Savings (20%) → ₹6,000

Example:

- Rent: ₹8,000

- Food: ₹5,000

- Transport: ₹3,000

- Bills: ₹2,000

Total = ₹18,000

Action:

Write your exact numbers today. Not tomorrow.

Step 2: Control Rent (Biggest Expense)

Rent eats your salary.

What to do:

- Share room/flat

- Move slightly outside prime area

- Avoid “status rent”

Example:

- Single room: ₹10,000

- Shared: ₹6,000

You save ₹4,000 instantly

Action:

If rent > 35% of income, fix this first.

Step 3: Fix Food Spending (Hidden Leak)

Swiggy and Zomato will kill your savings.

What to do:

- Cook 70% of meals

- Limit eating out to weekends

- Buy groceries weekly

Example:

- Ordering daily: ₹6,000/month

- Cooking: ₹3,500/month

You save ₹2,500

Action:

Track food spending for 7 days. You’ll see the problem.

Step 4: Automate Savings First

If you save “what’s left,” you’ll save nothing.

What to do:

- Set auto-transfer on salary day

- Move ₹3,000–₹6,000 immediately

Where to put:

- Savings account (short term)

- SIP (long term)

Action:

Set auto-debit today. No excuses.

Step 5: Cut These 3 Expenses Immediately

These look small. They aren’t.

1. Subscriptions

- OTT, apps, random tools

Cut or share accounts

2. Impulse Shopping

- Amazon “offers” trap

24-hour rule before buying

3. Daily Treat Spending

- Tea, snacks, random spends

Limit to fixed budget

Action:

Cancel at least 2 subscriptions today.

Step 6: Increase Income (Non-Negotiable)

Saving alone won’t work long-term.

Options:

- Freelancing (writing, design, editing)

- Instagram + small business

- Weekend gigs

Example:

Extra ₹5,000/month = double your savings

Action:

Pick one skill. Start within 7 days.

Real-Life Example (₹30,000 Salary Breakdown)

Rahul, 26, Chennai

Income: ₹30,000

| Category | Before | After |

| Rent | ₹10,000 | ₹6,000 |

| Food | ₹6,000 | ₹3,500 |

| Transport | ₹3,000 | ₹3,000 |

| Bills | ₹2,000 | ₹2,000 |

| Wants | ₹6,000 | ₹5,000 |

| Savings | ₹3,000 | ₹10,500 |

He increased savings from ₹3K → ₹10.5K

No magic. Just control.

Common Mistakes

- Saving after spending everything

- Living alone for “privacy”

- Ordering food daily

- Ignoring small subscriptions

- Not increasing income

Fix these, and you’re already ahead of 80% people.

Pro Tips

- Use UPI + separate account for expenses

- Withdraw weekly cash for control

- Review spending every Sunday

- Avoid EMIs unless necessary

- Increase savings every salary hike

To make this system easier:

- Use SIP apps like Groww or Zerodha Coin

- Open a high-interest savings account

- Try expense trackers like Walnut or Money Manager

These tools automate discipline. You don’t rely on willpower.

FAQ

1. Can I really save on ₹30,000 salary?

Yes. You can save ₹3,000–₹10,000 with proper control.

2. What is the ideal saving percentage?

Start with 10%. Aim for 20% or more.

3. Should I invest or just save?

Do both. Save for emergencies. Invest for growth.

4. How much emergency fund is needed?

At least 3–6 months of expenses.

5. Is SIP good for beginners?

Yes. It’s simple and builds discipline.

Conclusion

Saving money on ₹30,000 salary is not hard.

But it requires discipline.

Control rent. Fix food. Automate savings. Increase income.

Do these four things consistently, and your finances will change.

No hacks. No shortcuts. Just execution.