Earning ₹50,000 per month in India feels decent at first.

But many people still end up broke before month-end.

Why?

Because salary alone does not build wealth. Structure does.

If you earn ₹50K/month and want better savings, investments, insurance, and financial stability, this guide will show exactly what to do step by step.

No complicated finance jargon. Just practical money management that works in real Indian life.

Quick Answer: What Should You Do If You Earn ₹50K/Month in India?

Here’s the simple formula:

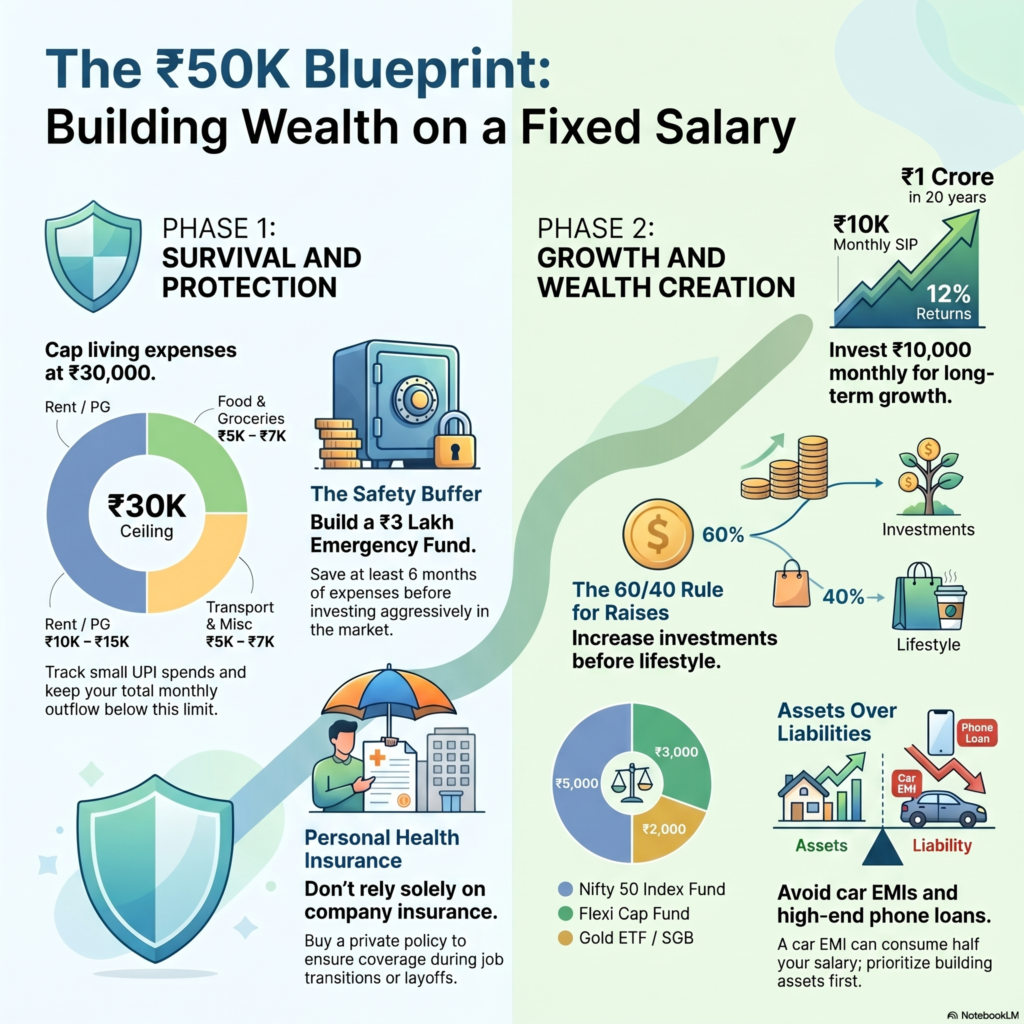

- Keep total living expenses below ₹30,000

- Build a ₹3 lakh emergency fund first

- Invest at least ₹10,000 monthly through SIPs

- Buy health insurance and term insurance

- Avoid EMI-heavy lifestyle upgrades

If you follow this consistently for 5–7 years, your financial situation changes completely.

Why ₹50K Salary Can Either Build Wealth or Destroy It

₹50K/month is a dangerous income level.

You earn enough to feel comfortable.

But not enough to survive careless spending.

This is where many people make mistakes:

- Expensive phones on EMI

- Unnecessary bike or car loans

- Weekend spending

- Credit card debt

- Zero investing

A person earning ₹35K with discipline often builds more wealth than someone earning ₹70K without a plan.

Your system matters more than your salary.

If You Earn ₹50K/Month in India — Follow This Exact Breakdown

1. Keep Monthly Expenses Around ₹25K–₹30K

This is the foundation.

If your expenses cross ₹35K regularly, saving becomes difficult.

Ideal expense split

| Category | Budget |

| Rent/PG | ₹10,000–₹15,000 |

| Food & groceries | ₹5,000–₹7,000 |

| Transport | ₹2,000–₹4,000 |

| Mobile/WiFi | ₹1,000 |

| Entertainment | ₹2,000 |

| Miscellaneous | ₹3,000 |

Action

Track spending for 30 days.

Use apps like:

- Walnut Money Manager

- Money Manager Expense & Budget

Most people underestimate small UPI spending.

That alone kills savings.

2. Build an Emergency Fund Before Investing Aggressively

If you earn ₹50K/month in India, your first target is not stocks.

It’s survival money.

How much?

At least 6 months of expenses.

If monthly expenses are ₹30K:

- Emergency fund target = ₹1.8 lakh

Safer target:

- ₹3 lakh

Keep this money in:

- High-interest savings account

- Liquid mutual fund

- Sweep FD

Why this matters

Without emergency savings:

- Job loss becomes a disaster

- Medical issues create debt

- Credit cards become your backup plan

That is financially dangerous.

3. Start SIP Investments Immediately

This is where long-term wealth actually starts.

If you invest ₹10,000 monthly from age 25:

At 12% annual return:

- After 10 years: roughly ₹23 lakh

- After 20 years: roughly ₹1 crore

That’s the power of consistency.

Best SIP allocation for beginners

| Investment | Monthly Amount |

| Nifty 50 Index Fund | ₹5,000 |

| Flexi Cap Fund | ₹3,000 |

| Gold ETF/SGB | ₹2,000 |

Good platforms

Don’t keep waiting for the “perfect time” to invest.

Most people delay for years.

4. Buy Health Insurance Immediately

A single hospitalization can destroy years of savings.

Company insurance is not enough.

Especially if:

- You switch jobs

- Lose your job

- Parents depend on you

Minimum coverage suggestion

| Person | Coverage |

| Single person | ₹5 lakh |

| Married | ₹10 lakh family floater |

Popular insurance platforms

Health insurance is boring until you need it.

Then it becomes the most important purchase you ever made.

5. Avoid Lifestyle Inflation

This is the biggest trap after salary increases.

You start earning ₹50K.

Suddenly:

- ₹1,500 dinners feel normal

- ₹80K phones look “necessary”

- BNPL apps become routine

Your income rises.

But your net worth stays zero.

Simple rule

Every salary hike should increase investments first.

Not expenses first.

Example:

- Salary increases by ₹10K

- Increase SIP by ₹6K

- Use remaining ₹4K for lifestyle improvements

That’s sustainable.

6. Don’t Buy a Car Too Early

This advice hurts people’s ego.

But financially, it’s true.

If you earn ₹50K/month in India, a car EMI can destroy your cash flow.

Example

| Expense | Amount |

| Car EMI | ₹12,000 |

| Fuel | ₹6,000 |

| Insurance/Maintenance | ₹3,000 |

Total:

- ₹21,000/month

That’s almost half your salary.

Unless absolutely necessary:

- Use bike

- Use metro

- Use Ola/Uber strategically

Build assets before liabilities.

7. Learn One Extra Income Skill

A ₹50K salary becomes powerful when combined with side income.

You do not need a business immediately.

You need a monetizable skill.

Good side skills in India

- Content writing

- Video editing

- Graphic design

- Coding

- SEO

- Performance marketing

- Freelancing

- YouTube scripting

Even ₹10K extra monthly changes your savings rate massively.

Where to learn

Real-Life Example: ₹50K Salary Breakdown in India

Let’s take a realistic example.

Rahul, age 28, Bangalore

Monthly salary

- ₹50,000 in hand

Monthly expenses

| Expense | Amount |

| Shared rent | ₹12,000 |

| Food | ₹6,000 |

| Transport | ₹3,000 |

| Utilities | ₹2,000 |

| Entertainment | ₹3,000 |

| Miscellaneous | ₹4,000 |

Total expenses:

- ₹30,000

Monthly investing

| Investment | Amount |

| SIPs | ₹10,000 |

| Emergency fund | ₹5,000 |

| Insurance | ₹2,000 |

| Skill learning | ₹3,000 |

Result:

- Financial stability improves within 1–2 years

- No debt stress

- Growing investments

- Better career opportunities

This is realistic.

Not some fake influencer budget.

Common Mistakes People Make After Reaching ₹50K Salary

1. Taking multiple EMIs

Phone EMI + bike EMI + credit card EMI = financial trap.

2. Delaying investments

People wait for “higher salary.”

That delay costs years of compounding.

3. Ignoring insurance

One medical emergency can wipe savings instantly.

4. Spending entire bonus

Bonuses should mostly build investments or emergency funds.

5. Depending on one income source

Job security today is weaker than most people think.

Pro Tips If You Earn ₹50K/Month in India

- Automate SIPs right after salary day

- Keep one separate account for bills

- Use credit cards only for rewards, not borrowing

- Increase investments every appraisal cycle

- Avoid personal loans unless absolutely necessary

Useful Financial Tools and Platforms

Investing

Budget Tracking

- Walnut

- Goodbudget

Insurance Comparison

Credit Score Tracking

FAQ: If You Earn ₹50K/Month in India

Is ₹50K salary good in India?

Yes, for a single person it is decent in most cities.

But poor money management can still create financial stress.

How much should I save from ₹50K salary?

Aim to save and invest at least 25%–35%.

That means roughly ₹12K–₹18K monthly.

Can I buy a car with ₹50K salary?

You can.

But it may slow wealth creation significantly.

A car makes sense only if it improves income or saves major time.

How much SIP should I start with?

Minimum:

- ₹5,000/month

Better:

- ₹10,000/month

Consistency matters more than amount initially.

Should I invest or build emergency fund first?

Build a small emergency fund first.

Then start SIPs alongside larger emergency savings.

Is health insurance necessary if company provides it?

Yes.

Employer insurance disappears when your job disappears.

Personal coverage is important.

Conclusion

If you earn ₹50K/month in India, you are in a strong position compared to many people.

But salary alone means nothing without structure.

Keep expenses controlled.

Invest consistently.

Avoid unnecessary EMIs.

Build emergency savings.

Increase income skills.

Most people earning ₹50K stay financially stuck because they upgrade lifestyle too fast.

The people who quietly build wealth usually do boring things consistently for years.